Key takeaways

- Branch transformation is 8 interlocking components, not one product: intake, routing, signage, kiosks, visitor management, wayfinding, feedback, and on-premises AI.

- For a 200-branch national bank, expect £600k-£2.5M build, £40k-£120k per integration system, and a 12-18 month rollout if you pilot properly.

- The biggest cost driver is not software or hardware; it is vendor count. One ecosystem replaces 5 integration projects with 1.

- Skill-based routing alone lifts teller utilisation 12-18 points and cuts service time 25-40% at branches with no formal queueing discipline.

- Self-service kiosks deflect 35-55% of non-advisory transactions when staff are retrained to triage at the door.

- Sovereign on-premises is not optional under GDPR + PDPL + NCA-ECC simultaneously; cloud-only branch SaaS fails the data-residency test on day one.

- A defensible 200-branch business case lands at £15M-£40M net 5-year benefit, dominated by FTE redeployment and kiosk deflection.

This guide is written for retail banking executives scoping branch transformation as a single operating-model decision, not as a procurement of seven unrelated tools. It covers the eight components, the integration map into core banking and CRM, realistic pricing bands, an ROI calculator you can defend in front of a board, and the seven failure modes we have seen wreck multi-million-pound rollouts. It is the conversation the Zeour engineering team has with a bank's COO before contract, written down.

Who this guide is for

- Retail Banking COO. You run 50-500 branches across one or several markets. The board has a mandate for branch experience but your per-branch operating cost target has not moved in five years. You need the architecture that lifts both at once.

- Branch Network Director. You run 200-1,000 branches across regions with mixed regulation — GDPR, PDPL, NCA-ECC. You need a single platform with per-region tenanting and data residency you can prove to a regulator without a slide deck.

- Head of Retail Distribution Strategy. You are evaluating a branch-of-the-future pilot and your CFO wants to know which combination of QMS, virtual queueing, appointments, kiosks, signage, and feedback actually moves NPS and reduces opex.

- CIO at a Tier-1 bank. You are scoping the integration map: core banking (Temenos / Finacle / Mambu), CRM (Salesforce / Dynamics), identity (SAML / OIDC), ITSM, data warehouse. You need a vendor whose APIs survive contact with your existing rails.

What is branch transformation in 2026?

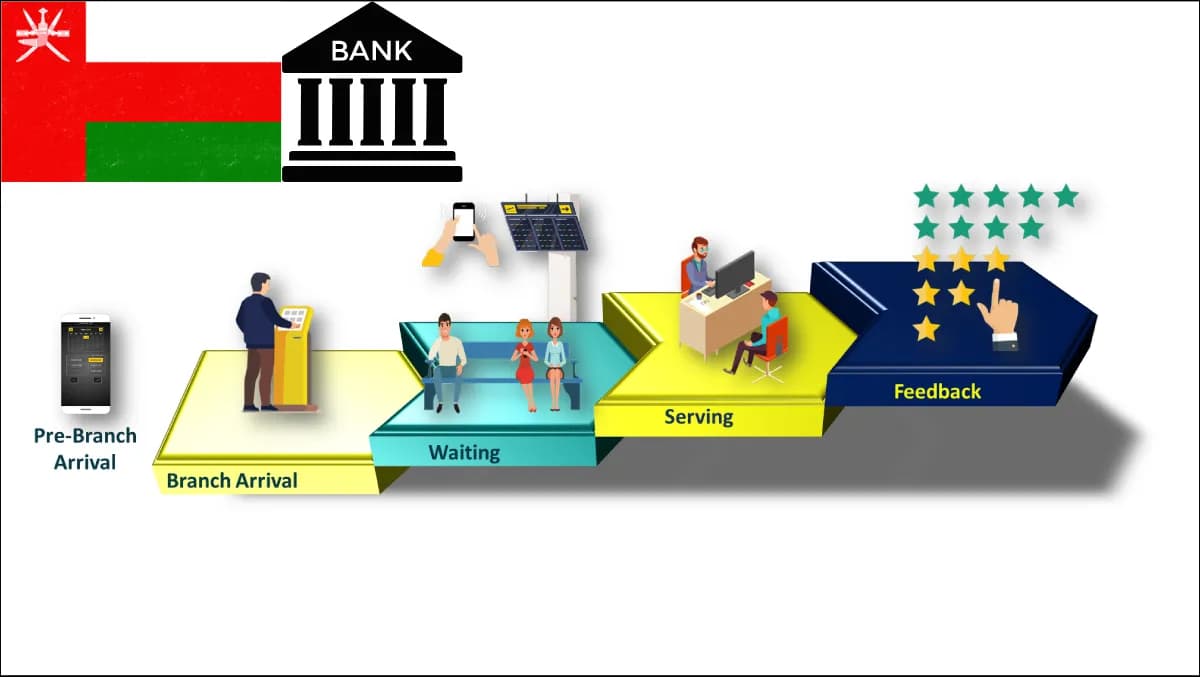

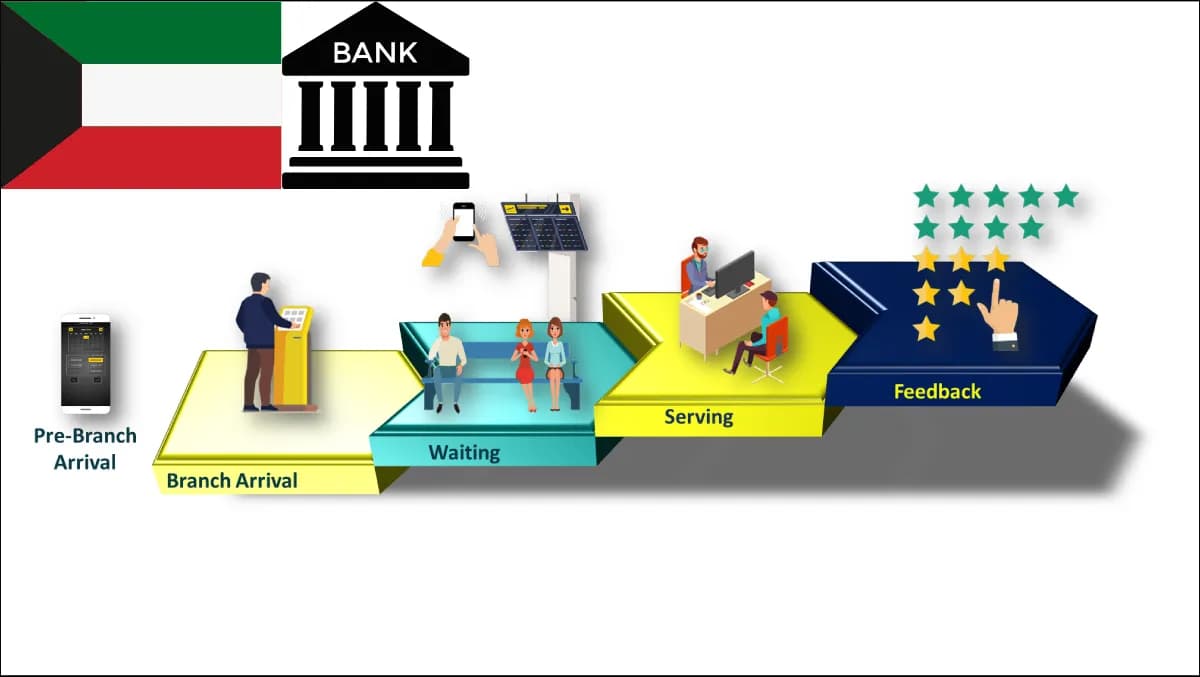

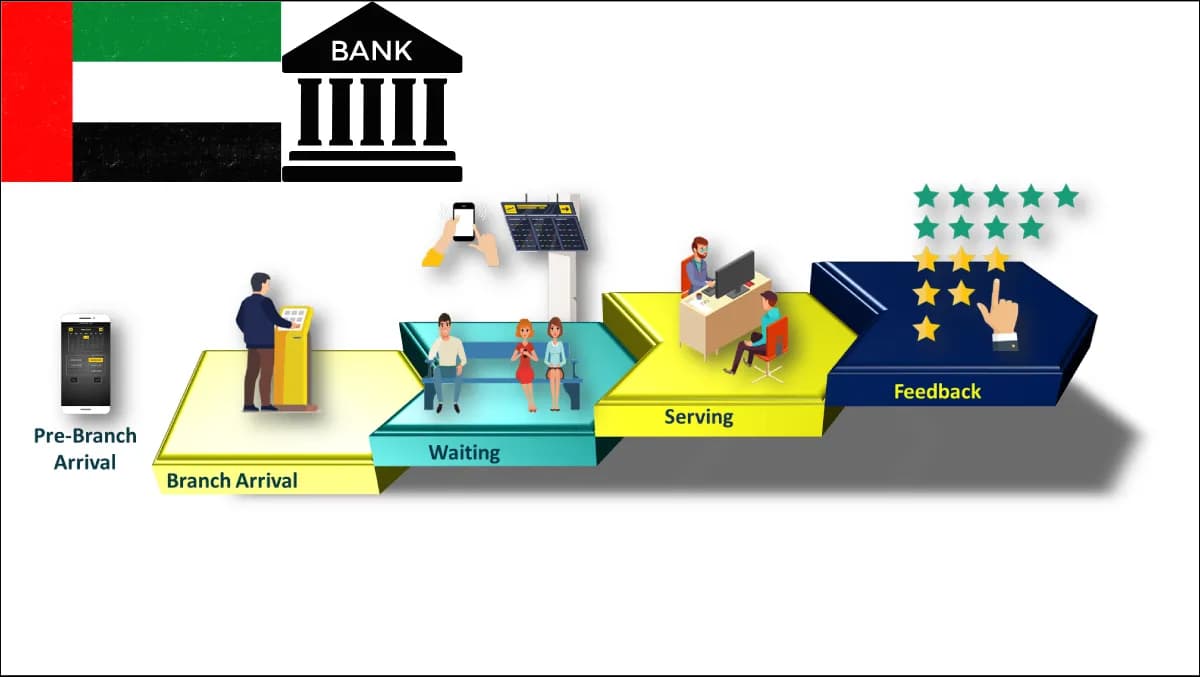

Branch transformation in 2026 is the deliberate redesign of how a retail bank uses its physical estate, given that 70-85% of routine transactions have already moved to mobile and online channels. The branch is no longer the transaction venue; it is the advice venue, the compliance venue, and the deflection venue for everything that cannot be done in an app. A programme is the operating-model change that aligns staffing, technology, layout, and process to that reality.

Technically, the programme is the integration of a queue management system, a virtual queueing layer, an online appointment surface, a self-service kiosk fleet, a visitor management workflow, a wayfinding system for multi-floor sites, a digital signage CMS, and a customer feedback loop wired to the branch event stream. Increasingly, an on-premises AI layer sits underneath, providing advisor co-pilot, complaint triage, and document understanding without sending customer records to a public-cloud LLM API.

What separates a real programme from shelfware is whether the components share one schema, one identity surface, and one operator. If your QMS does not know what your appointment system knows, customers are asked their name three times. If your signage does not subscribe to the QMS event bus, you pay a vendor to display content nobody updates. The discipline is integration density — the fewer vendor seams, the faster the lift. Banks that get this right treat transformation as a five-year programme with fixed-fee Discovery, a pilot, a regional cluster, and a national estate rollout in that order. Banks that get it wrong treat it as a procurement exercise and discover 18 months in that integration cost exceeds the original software bill.

The 8 components of a real branch transformation programme

Every serious branch transformation programme is made of the same eight components. Skip one and the others do less than they should.

1. Multi-channel customer intake

What and why. A unified intake surface across kiosk, walk-in, virtual queue (WhatsApp / SMS / web), and online appointment with one ticket schema. Walk-in-only intake means peak-hour crowding and impossible-to-staff variance; multi-channel spreads arrivals so staffing matches real demand.

Zeour solution. Queue management + virtual queue + online appointment — one schema, one identity surface. See the virtual queueing implementation guide.

Core banking integration. Customer lookup via core banking API (Temenos T24 / Finacle FI / Mambu) at ticket-create to resolve CIF and tier. Appointment write-back to Salesforce Financial Services Cloud or Dynamics 365. SAML / OIDC for advisor login.

Skip it and the lobby floods at peak even when every other component is in place.

2. Skill-based routing and branch flow

What and why. The QMS routing engine deciding which counter the next customer goes to, based on service, counter skills, tier, appointment, and load. Without skill-based routing, premium customers wait behind cheque-deposit walk-ins; with it, teller utilisation lifts 12-18 points and average service time drops 25-40%.

Zeour solution. GLARUS queue management with tier-aware rules, advisor calendars, per-branch overrides. See the queue management buyer's guide.

Core banking integration. Real-time tier read from core. Service-catalogue alignment with CRM.

Skip it and the QMS prints tickets but routes them FIFO. NPS does not move.

3. Branch signage and audio call-forward

What and why. A digital signage CMS running every screen — counter-call, lobby summary, advisor-availability, queue-status TVs — driven by one event bus. Without it, the QMS shouts "Ticket B-47" into the void; with it, the next ticket lights up on the correct counter.

Zeour solution. GRAVIA digital signage system — multi-tenant CMS subscribing to GLARUS QMS events, bilingual EN / AR out of the box. See the digital signage CMS buyer's guide.

Core banking integration. QMS event subscription. Optional feed from the bank's marketing CMS for brand-approved promotional zones.

Skip it and screens become decoration. Staff still call tickets verbally.

4. Self-service kiosks

What and why. In-branch kiosks for non-advisory transactions — card pickup, cheque deposit, account servicing, statement printing, PIN reset, CIF onboarding. Kiosks deflect 35-55% of non-advisory transactions when staff are retrained to triage at the door.

Zeour solution. GLARUS self-service kiosk on Android with Ingenico / PAX / Verifone payment, Epson / Star Micronics printers, ZKTeco / Suprema biometric capture. See the kiosk TCO guide.

Core banking integration. Direct call into core for balance enquiry, statement generation, card-issuance. Identity via SAML or the bank's strong-customer-authentication broker.

Skip it and branch retains 100% of routine transactions at the teller line. Cannot redeploy a single FTE.

5. Visitor management

What and why. A visitor management system for advisor appointments, corporate clients, contractors, and regulators — pre-registration, ID capture, NDA acceptance, badge printing, host notification. A clipboard process fails the audit-trail test under GDPR and PDPL.

Zeour solution. GLARUS visitor management. See the visitor management compliance guide and the enterprise visitor check-in workflow.

Core banking integration. Advisor calendar sync from Microsoft 365. Host directory sync from Active Directory. CRM write-back for relationship-manager visits.

Skip it and the bank fails its next audit when the regulator asks for a contractor access log. Retrofit costs 3x.

6. Wayfinding

What and why. Wayfinding for multi-floor branches, flagship sites, and HQ campuses — interactive directories, route guidance to counters or advisor desks, meeting-room finders. Closes the gap between "I have an appointment with Mortgages" and "floor 3, desk 14."

Zeour solution. GLARUS wayfinding — integrates with QMS to flash a route on counter-call, WCAG-compliant. See the interactive wayfinding buyer's guide.

Core banking integration. Advisor desk metadata sync from HR / facilities. Read-only floorplan ingest. Optional meeting-room booking integration.

Skip it and nothing for small high-street branches; mandatory only for flagships over 800 m squared and HQ buildings.

7. Customer feedback loop

What and why. A feedback system wired directly to the QMS event stream so every served ticket generates a contextual survey at the counter, via SMS, in-app, or QR. Without it, branch experience is measured via a quarterly survey nobody can act on; with it, per-counter, per-advisor CSAT and NPS within a working day.

Zeour solution. GLARUS customer feedback — kiosk + SMS + web + advisor panel, subscribing to QMS events natively.

Core banking integration. QMS event subscription. Optional CRM write-back so low NPS triggers a relationship-manager follow-up. Optional feed to HR performance system.

Skip it and the bank has no signal that transformation worked. CFO refuses to fund phase two.

8. On-premises AI

What and why. An on-premises AI layer running open-weight LLMs (Llama / Mistral / Mixtral / Qwen / DeepSeek) on the bank's hardware via vLLM, Ollama or TGI, with retrieval-augmented generation over product manuals, compliance policies, and complaint corpus. Advisor co-pilot, complaint triage, and KYC document understanding cannot send customer records to a public-cloud LLM API under any sovereign regime.

Zeour solution. Digital transformation consultation and enterprise development services. See the on-premises LLM deployment guide.

Core banking integration. Read-only ingest from the bank's document store. Optional CRM write-back when co-pilot drafts a complaint response. Air-gapped option for the strictest regulators.

Skip it and the bank cannot lift advisor productivity beyond desk-side training. Competitors with co-pilots widen the gap quarter on quarter.

How do you choose between an all-in ecosystem, best-of-breed stitched, and cloud-only branch SaaS?

The three postures look similar in a procurement matrix and produce wildly different five-year outcomes.

| Decision factor | All-in operator-hosted ecosystem | Best-of-breed stitched | Cloud-only branch SaaS |

|---|---|---|---|

| Data residency | Operator controls; per-region tenanting; meets GDPR + PDPL + NCA-ECC simultaneously | Depends on each vendor; usually fails at least one regime | Vendor-controlled; typically fails sovereign data-residency tests |

| Integration cost | 1 integration project across all 8 components | 5-7 projects, one per vendor | 1 project, limited to vendor API surface |

| Time-to-rollout per branch | 2-4 days post-pilot | 8-14 days per branch | 1-2 days but limited depth |

| 5-yr TCO at 200 branches | £3M-£6M | £5M-£12M (vendor sprawl) | £4M-£8M (monthly fees compound) |

| Exit posture | Operator owns repo, licence, deploy keys; 90-day exit window | Multi-vendor lock-in | Hard lock-in; egress fees, proprietary schemas |

| Operation when WAN drops | Branches keep operating on local infrastructure | Mixed; depends which vendor cloud is down | Branches stop accepting tickets |

The all-in ecosystem wins decisively for any bank above 50 branches or across more than one regulatory regime. The cost of stitching five or six vendors compounds at every renewal, every API version bump, and every regulator-driven schema change. Cloud-only is a non-starter under NCA-ECC or local PDPL, and a hidden cost trap even where regulation allows it. Best-of-breed makes sense only when the bank is already committed to a point solution it cannot replace.

Want a fixed-fee Discovery price before the end of the call? Talk to Zeour engineering — 30-minute scoping conversation, no slideware, and a published pricing band by the time we hang up.

How much does branch transformation cost in 2026?

Budget is a function of estate size, integration count, and whether the bank is consolidating from a legacy vendor estate or starting greenfield. Bands we publish before signature:

- Discovery (fixed-fee): £20k-£50k for multi-branch scoping. Covers the eight-component map, integration spec, per-region data-residency plan, and a costed phased rollout proposal. Always fixed-fee at Zeour.

- Build (small): £150k-£400k for a single-brand 20-50 branch programme covering 4-6 of the 8 components with one regulatory regime.

- Build (enterprise): £600k-£2.5M for a national 200-1,000 branch rollout covering all 8 components, multi-region tenanting, and bilingual EN / AR baseline.

- Integrate: £40k-£120k per integration system (core banking, CRM, identity, ITSM, data warehouse). Budget for 4-7 systems on a Tier-1 build.

- Pilot: £40k-£100k for a 1-5 branch pilot with full instrumentation and weekly demos.

- Care Plan: tiered by branch count and SLA. Typical 200-branch bank lands at £180k-£480k annual.

- Per-branch hardware: £8k-£25k depending on kiosk count, screens, ticket printers, biometric capture, and signage real estate.

ROI calculator — build a defensible business case in 7 steps

The board wants one number: net 5-year benefit. The CFO wants the formula. Here is the calculation that survives audit.

Step 1: Wait-time recovery

(average wait reduction in minutes) × (annual visits per branch) × (value per customer hour) × (branches). Typical: 8 × 40,000 × £15 × 200 = £16M / year of customer time recovered. Discount heavily; defensible cases use 15-25% of gross.

Step 2: Staff utilisation lift via routing

(teller utilisation lift in points) × (fully loaded teller cost) × (tellers per branch) × (branches). Typical: 14 × £42k × 4 × 200 = £4.7M annual capacity unlocked.

Step 3: Self-service deflection

(deflected transactions per branch per year) × (per-transaction labour cost) × (branches). Typical: 18,000 × £2.40 × 200 = £8.6M annual labour saving.

Step 4: NPS uplift and customer lifetime value

(NPS point lift) × (LTV uplift per point) × (active customers per branch) × (branches). Typical: 9 × £4 × 18,000 × 200 = £130M nominal; defensible cases recognise 5-10%.

Step 5: Advisor capacity unlocked

(advisor hours unlocked per week via appointments + co-pilot) × 52 × (advisor revenue per hour) × (advisors per branch) × (branches). Typical: 6 × 52 × £180 × 3 × 200 = £33.6M revenue capacity, recognised at the bank's actual advisor conversion rate.

Step 6: Compliance audit cost reduction

(audit hours saved per branch per year) × (audit hourly cost) × (branches). Typical: 24 × £220 × 200 = £1.05M saved from automated visitor logs, feedback trails, and event-sourced QMS data.

Step 7: Per-branch headcount reallocation

(FTE redeployed per branch) × (fully loaded FTE cost) × (branches). Typical: 1.2 × £48k × 200 = £11.5M annual — the largest single contributor and the most defensible because it shows up in payroll. See the digital service transformation ROI playbook for redeployment-vs-redundancy framing.

Worked example. A 200-branch national bank running the full eight-component programme lands at £15M-£40M net 5-year benefit, dominated by FTE redeployment and self-service deflection, against £6M-£10M total programme cost. Defensible cases use the low end and still clear board hurdle rates.

Seven failure modes from real deployments

Failure mode 1: Procuring QMS without virtual queueing. The bank installs a ticket-printer QMS and the lobby still floods at peak because customers must be physically present to take a number. Fix: scope virtual queueing on day one.

Failure mode 2: Choosing one solution per vendor. Separate QMS, signage, kiosk, and feedback vendors mean integration is five projects instead of one. Fix: insist on ecosystem unity at RFP scoring; integration density should weigh at least 25% of vendor selection.

Failure mode 3: Cloud-only deployment where regulation forbids it. The bank signs cloud-only SaaS and is told 14 months in the regulator requires data residency the vendor cannot provide. Fix: do the data-residency map in Discovery. Sovereign on-premises is the default under PDPL or NCA-ECC.

Failure mode 4: Self-service kiosks installed without staff retrain. 800 kiosks are used 8% of the time because door staff still direct customers to the teller line. Fix: invest in concierge retraining as part of the rollout budget. Kiosk deflection is a behavioural lift, not a hardware lift.

Failure mode 5: No customer feedback loop. The bank invests £4M in transformation and has no per-counter, per-advisor signal it worked. CFO refuses phase two. Fix: wire customer feedback to the QMS event bus on day one.

Failure mode 6: Vendor lock-in with no exit window. No exit clause, no source-code escrow, proprietary schema. Five years in, renewal pricing doubles. Fix: insist on a 90-day exit window and operator ownership of the repo, licence, and deploy keys. The Zeour default.

Failure mode 7: Treating transformation as a tech project, not an operating-model change. IT runs the programme, the branch network changes no processes, and technology lands on top of a workflow it was never designed for. Fix: the programme reports to the COO, not the CIO. Branch managers are co-designers from Discovery.

Migration path — moving from your current stack

Phase A: Single-branch pilot of the full stack. Pick one branch — ideally a flagship with mixed traffic — and deploy all eight components in 8-12 weeks. Instrument everything: ticket volumes, service times, NPS per advisor, kiosk deflection, abandonment. The pilot validates integration, not demand.

Phase B: Cluster rollout (5-10 branches). Take the validated pilot to a regional cluster at one branch per fortnight. Each branch is now a 2-4 day cutover, not a 12-week project. The cluster phase exposes per-branch variance and lets you tune the operating model before estate scale.

Phase C: Estate rollout at 5-10 branches per week. Cluster discipline lets the programme scale with a single deployment squad and per-branch retrain. A 200-branch estate completes in 8-12 months. A 1,000-branch estate completes in 24-36 months with two squads in parallel and a regional pattern following the bank's district structure.

Phase D: Multi-region multi-tenant consolidation at corporate. Once estate rollout completes, the multi-tenant platform consolidates per-region reporting into one corporate operations view. Per-region tenancy preserves data residency; the corporate view aggregates metrics without aggregating data. On-premises AI complaint triage and advisor co-pilot land at scale here.

Implementation playbook

- 1Discovery (2-4 weeks). Fixed-fee. Eight-component map, integration spec, per-region data-residency plan, costed phased rollout, signed scope document.

- 2Build (8-16 weeks). Pilot-branch implementation, integration build-out, bilingual UI configuration, hardware procurement, staff training plan.

- 3Integrate (3-5 weeks). Core banking adapter, CRM write-back, identity broker, ITSM ticket flow, data warehouse feeds. Run in parallel with Build where possible.

- 4Pilot and go-live (4 weeks). Single-branch pilot, weekly demos to the steering committee, daily standups with branch staff, instrumented baseline.

- 5Operate. Care plan engagement, monthly operations review with the COO's office, quarterly capacity planning, annual roadmap with the operator.

Frequently asked questions

What is branch transformation in 2026 — and how is it different from a tech refresh?

Branch transformation is an operating-model change wrapped around a technology programme; a tech refresh is a hardware replacement cycle. The first re-baselines per-branch unit economics by combining the eight components into one platform. The second swaps old kiosks for new at the same per-transaction cost.

How long should a 200-branch national rollout actually take?

A well-run programme takes 14-20 months: 3-4 weeks Discovery, 10-14 weeks Build and Integrate in parallel, 4 weeks Pilot, 4 months Cluster, 8-10 months Estate at 5-7 branches per week. Programmes that exceed 24 months almost always failed at the Cluster phase by skipping per-branch tuning.

Which solution should we deploy first?

Queue management plus virtual queueing in the same release, then signage in the same pilot. Kiosks and feedback land at the cluster phase once intake is stable. Visitor management runs as a parallel track. Wayfinding is reserved for flagships and HQ. On-premises AI lands once the estate has predictable event data.

How do you integrate with core banking (Temenos, Finacle, Mambu)?

Via the bank's existing integration broker. Zeour QMS, kiosks, and feedback components read CIF, tier, and product holdings at ticket-create and transaction-start, and write back appointment-completed, service-rendered, and feedback-captured events. For Temenos T24 we use IRIS or Java adapters; Finacle FI uses Connect24; Mambu uses REST directly. Identity via SAML or OIDC against the bank's IdP.

Should branch transformation live with Operations or IT?

Operations. The COO owns the outcome; the CIO owns delivery. When the programme reports into IT, branch processes never change. When it reports into Operations, branch managers are co-designers from Discovery and the operating model shifts in step. Every successful programme we have shipped reported into Operations with delivery inside IT.

How do you handle data residency across multiple regulatory regimes?

Per-region tenancy on operator-controlled infrastructure. Each region runs its own instance with its own database, backup posture, and audit log. The corporate view aggregates metrics, not data. The only architecture that survives a GDPR + PDPL + NCA-ECC audit simultaneously, and why sovereign deployment is the Zeour default.

What's the realistic FTE redeployment per branch?

0.8-1.8 FTE per branch over an 18-month window after go-live. Banks on ticket-printer-only QMS land at the high end; banks already running kiosks land at the low end. Redeployment is mostly teller capacity moving to advisory roles, not redundancies — communicate that early.

How do you measure branch transformation ROI for the board?

Report six numbers monthly: average wait time, abandonment rate, NPS, kiosk deflection rate, teller utilisation, advisor capacity utilised. Report two quarterly: FTE redeployed and net cost per served customer. Avoid maturity scores — the board wants delta against pre-pilot baseline.

How does on-premises AI fit into branch operations?

Three initial use cases: advisor co-pilot (product fit, draft response, summarise policy), complaint triage (classify, prioritise, route, draft acknowledgement), and document understanding (parse KYC packs, extract data, flag exceptions). All run on the bank's hardware via vLLM or Ollama against open-weight LLMs grounded by RAG. Zero customer data leaves the perimeter.

What does a Zeour branch transformation deployment look like at a 200-branch bank?

Fixed-fee Discovery in week one. Pilot live by week 14. Cluster of 6 branches by month 6. Estate at 5 branches per week from month 8, completing at month 16. Operator owns the repo, licence, and deploy keys at every milestone; the 90-day exit window is in the contract from day one. Reference deployments include retail banks across UK, EU, GCC, and MENA — see Kuwait National Bank, London, IIB Bank, and Aljanoob Bank.

Where Zeour fits

Zeour ships the full eight-component branch transformation stack as one platform: GLARUS queue management, virtual queue, online appointment, self-service kiosk, visitor management, wayfinding, and customer feedback; GRAVIA digital signage; and digital transformation consultation for on-premises AI. Every engagement is fixed-fee phased, sovereign on-premises by default, bilingual EN / AR as production baseline, and shipped with a 90-day exit window that hands the operator the repo, licence, and deploy keys. Worldwide delivery from London with regional strength across UK, EU, Americas, GCC, MENA, Africa, and Asia. Book a 30-minute scoping call, browse pricing bands, or read the wider Zeour blog.

---

Last updated: May 17, 2026 — by the Zeour engineering team.