Key takeaways

- Kuwait bank branches sit under a tight regulatory perimeter: CBK, CITRA's Data Privacy Protection Regulation, and Kuwait Banking Association cybersecurity guidelines all touch how branch data flows.

- Kuwait Vision 2035 (New Kuwait) frames branch modernisation as a digital-economy programme. Boards expect the queue platform to feed measurable customer-experience KPIs, not just shorter lines.

- A defensible 2026 spec is bilingual English plus Arabic with full right-to-left, sovereign on-premises by default, KYC-aware ticketing tied to core banking, and an explicit 90-day operator exit window.

- Kuwait is a smaller market than KSA or UAE, which compresses cost bands. Build engagements for a mid-size network land between £80k-£250k; enterprise programmes between £300k-£1M.

- A Zeour-aligned queue management system ships with Arabic full-RTL and English as the production baseline, with other languages added per engagement.

- Production proof matters. The Kuwait-branded private bank we serve in London (read the case study) and Zeour's 1,247+ branches across 40+ countries short-circuit procurement reference checks.

- Avoid public-cloud-only SaaS for branch identity capture under CBK supervision: residency questions are easier when the platform runs inside your perimeter.

If you run a Kuwait retail-banking network and are scoping a 2026 programme under CBK and CITRA scrutiny, this is the field manual. It is written by engineers who have shipped queue, virtual-queue, appointment, kiosk, and visitor-management systems into banks across the GCC, MENA, Europe, and Asia, and references the /industries/banking playbook.

Who this guide is for

This guide targets four roles inside a Kuwait bank or Kuwait-incorporated financial institution.

The branch-network director running 20-100 branches. You own the physical estate. Wait-time is a top-three KPI. You want a live branch-by-branch dashboard, fair routing across teller windows, and proof you can show the regional manager weekly.

The CIO of a CBK-supervised bank. Sovereign data residency, integration to your core banking system, alignment to the CBK cybersecurity framework, and a clean answer to CITRA's Data Privacy Protection Regulation are non-negotiable. You want the platform to drop into your existing identity, SSO, and monitoring stack without a separate cloud account.

The head of retail experience. You want the queue platform to feed customer feedback scores into the same dashboard as branch NPS and complaint volumes, the digital signage above the teller floor to look like your brand, and the appointment booking flow to reach your wealth, mortgage, and SME segments cleanly.

The Vision 2035 transformation lead. You report into the executive committee on the bank's contribution to New Kuwait. You need a partner who can deliver in fixed-fee phases, hand over the keys at the end, and produce customer-experience uplift you can put in the annual report. A fixed-fee phased engagement with a defined 90-day exit window is your default expectation.

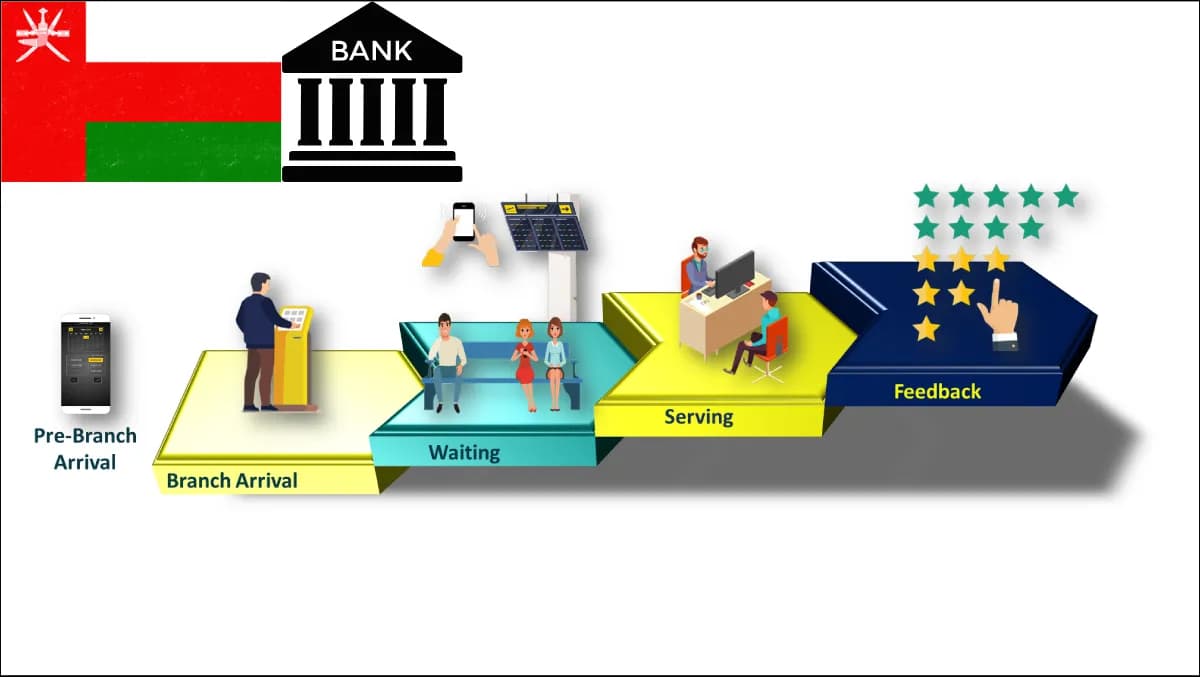

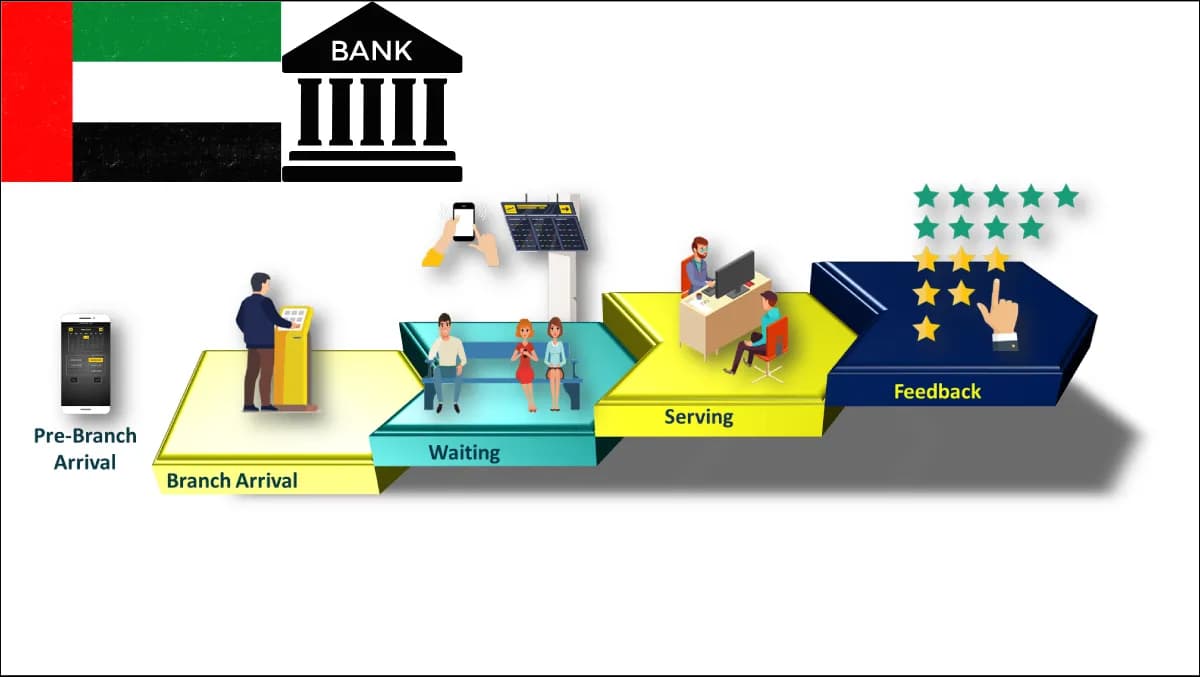

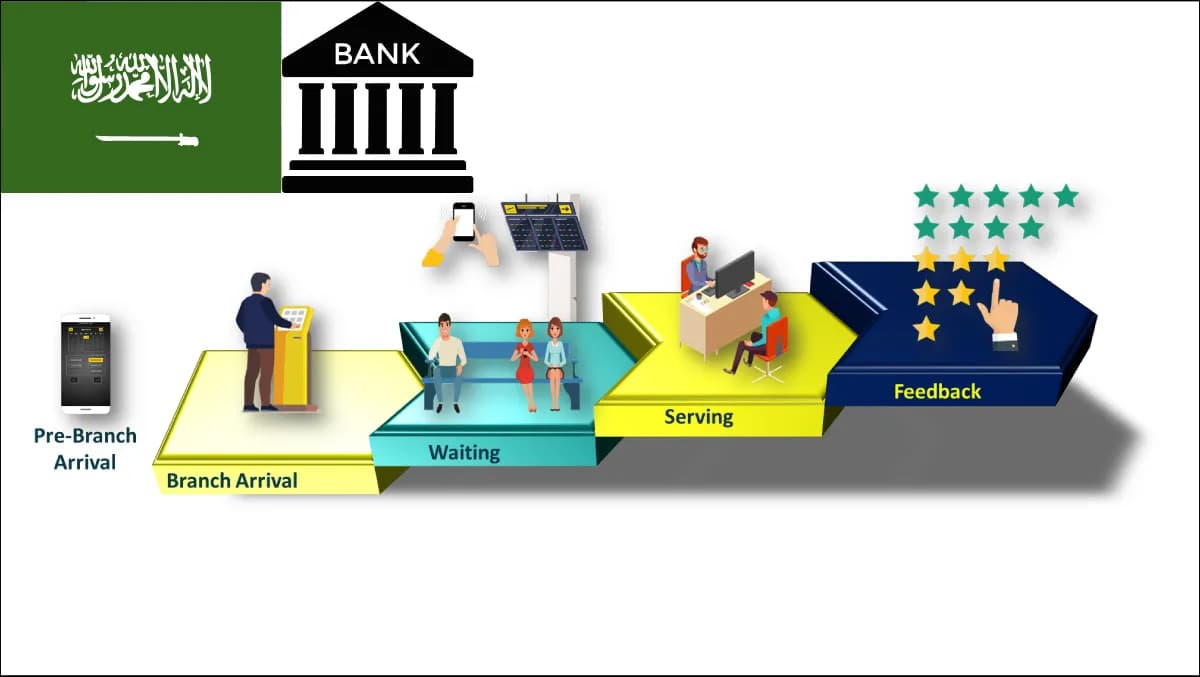

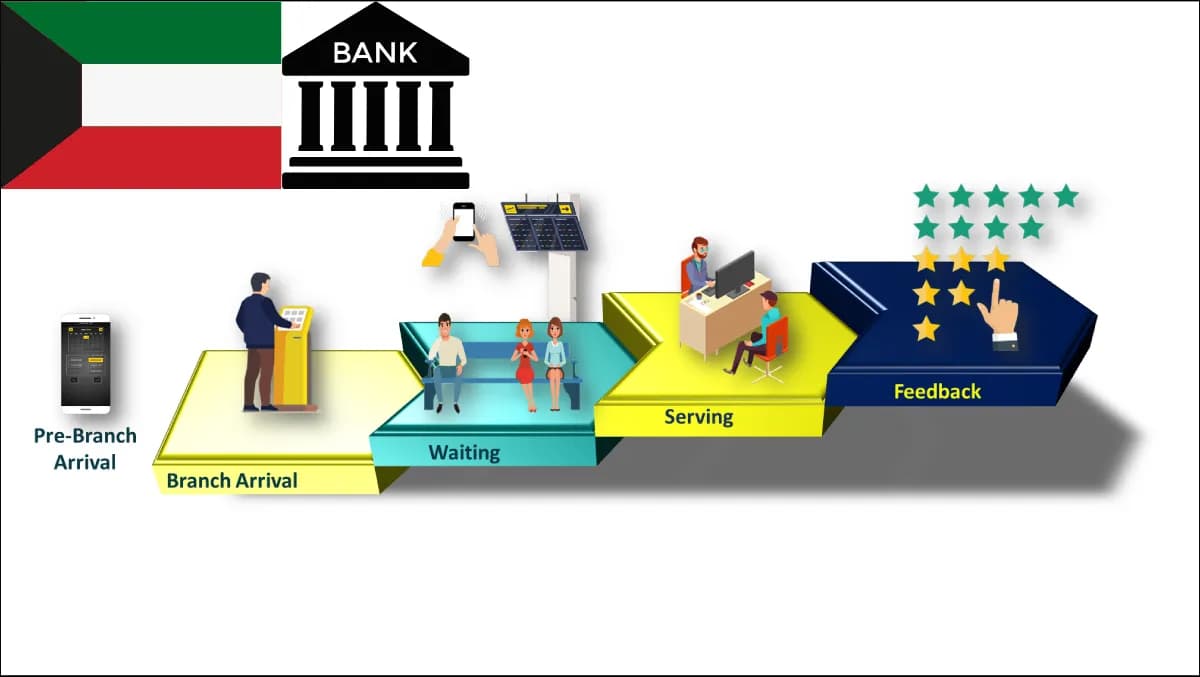

What is queue management in 2026 — and why it's different for Kuwait?

A modern queue management system is no longer a ticket printer plus a TV screen. By 2026 it is a branch-experience platform: ticket issuance across kiosk, mobile, WhatsApp, and staff devices; service-aware routing to the right teller or relationship manager; live wait-time forecasts; appointment overlay blending walk-ins with pre-booked visitors; and a data layer feeding analytics, complaints, and regulatory reporting.

For Kuwait the global pattern bends in five ways.

First, Arabic with full right-to-left is mandatory, not a customisation. Every screen — kiosk, signage, agent console, mobile ticket, SMS — must render in correct mirrored RTL with proper diacritics. This is the bilingual baseline: EN plus AR full RTL ship together as the production default.

Second, identity is regulated. CBK's KYC and AML rules constrain what you capture at a kiosk, how you store it, and how long. The platform must integrate with the national identity gateway pattern, and must let the operator decide which fields are mandatory, optional, or never collected at the kiosk.

Third, data residency is sharper. CITRA's Data Privacy Protection Regulation (the regional PDPL-equivalent) plus sector-specific CBK guidance makes "data leaves the country" a question the CISO must answer before signing. A sovereign on-premises deployment is the cleanest defensible posture.

Fourth, the appointment overlay matters more than in larger markets. Kuwait's branch density is high relative to population. The bank's challenge is to channel high-value visits (mortgage, business banking, wealth) into appointments at the right branch. A clean online appointment system earns its keep here.

Fifth, the digital-self-service layer is operational, not optional. Cash-deposit, cheque-deposit, statement-print, and card-issuance through a self-service kiosk move 30-50% of routine traffic off the teller floor — changing the queue maths upstream.

The Kuwait-fit scoring rubric — 14 criteria

Use this in the RFP. Score each vendor 1-5; a defensible 2026 platform scores 55+ out of 70.

| Criterion | What to score | Weight |

|---|---|---|

| Bilingual EN+AR RTL baseline | Production-grade Arabic mirroring on every surface | 5 |

| CBK alignment | Documented mapping to CBK cybersecurity framework controls | 5 |

| CITRA data-privacy posture | Explicit answer to Kuwait Data Privacy Protection Regulation | 5 |

| Sovereign on-prem deployment | Runs fully inside the bank perimeter; no mandatory outbound | 5 |

| Core-banking integration | Native connectors to Temenos, Finacle, Mambu, or in-house core | 4 |

| Identity-capture flexibility | Operator decides mandatory vs optional fields per service | 4 |

| Appointment overlay | Walk-in plus pre-booked blended fairly without queue-jumping | 4 |

| Kiosk + signage native | Same platform owns ticket kiosk and floor signage | 4 |

| Mobile + WhatsApp ticketing | Customer can join from phone, see position, get nudged back | 4 |

| Operator self-sufficiency | Operator runs the platform after exit; no licence captivity | 4 |

| Fixed-fee phased delivery | Discovery, Build, Care priced and scoped separately | 4 |

| 90-day exit window | Contract codifies handover of repo, runbooks, keys at end | 4 |

| Production references in region | At least 3 named deployments in GCC / MENA | 4 |

| Audit + reporting | Per-branch, per-service, per-staff dashboards with PDF/CSV export | 4 |

Anything under 45 is a non-starter under CBK and CITRA scrutiny in 2026. The /industries/banking play and the parallel KSA banks guide give the rubric for the larger market.

How do you choose between on-premises, sovereign cloud, and public-cloud SaaS in Kuwait?

Three deployment models are on the table.

On-premises inside the bank. The platform runs on bank-owned hardware in the bank's data centre. Database, identity capture, integration, and reporting all sit behind the existing firewall and monitoring stack. This is the cleanest CBK and CITRA posture and the default we recommend. Trade-off: hardware capex up front and the operations team must run the platform after exit (which is why we ship runbooks and training as part of the engagement).

Sovereign cloud in-country. The platform runs in a Kuwait-hosted region or a CITRA-aligned co-location. Data does not leave the country. Trade-off: contractual chain to the cloud provider; CBK questions on hypervisor isolation, key management, and operator access need clean answers.

Public-cloud SaaS. The vendor runs the platform in their global cloud region. Identity capture flowing to a foreign cloud region triggers a regulatory conversation most CIOs prefer to avoid. We do not recommend public-cloud SaaS for the regulated identity-capture path in 2026 Kuwait banking.

Our default for a CBK-supervised bank is sovereign on-premises, with sovereign cloud as a discussed alternative for non-regulated peripheral surfaces.

> Field note. When a CBK-supervised bank asked us in 2025 to map every data flow inside the queue platform to a CITRA Data Privacy Protection Regulation article, the on-prem deployment took 11 working days end-to-end. A public-cloud variant would have required a cross-border-transfer addendum, sub-processor review, and key-management attestation — none of which was needed because nothing left the bank. That is the operational meaning of sovereign on-premises by default.

How much does queue management cost in Kuwait in 2026?

Zeour invoices in pounds from London; we quote in Kuwaiti dinar for local convenience.

| Engagement phase | Typical range (£) | What it includes |

|---|---|---|

| Discovery | £15k-£40k | Branch-by-branch as-is mapping, stakeholder workshops, regulator-aligned spec, fixed-fee Build scope |

| Build — small network (5-20 branches) | £80k-£250k | Platform build, kiosk + signage + agent UI, core-banking integration, EN+AR baseline, deploy + UAT |

| Build — enterprise network (40-100 branches) | £300k-£1M | Above plus multi-region rollout, advanced reporting, appointment + mobile + WhatsApp channels |

| Per-system integration | £25k-£80k each | Core banking, CRM, identity gateway, signage, kiosk hardware (Ingenico, PAX, Verifone for card-present) |

| Per-branch hardware | £8k-£25k | Kiosks, ticket printers, floor signage screens, agent buzzer, network |

| Care plan (year 2+) | £30k-£120k/yr | Operator-side support, quarterly upgrades, on-call SLA |

The Kuwait market is smaller than KSA or UAE, which compresses cost bands. The parallel KSA banks guide gives you the larger-market comparators.

For how the deployment plays out for a Kuwait-branded bank, see our Kuwait National Bank London case study. For an adjacent regional state-bank reference, see the Aljanoob Bank deployment.

Discovery is fixed-fee and the only phase we sell standalone. It produces the spec the Build is priced against. A bank asking for a Build proposal without Discovery is asking us to guess; we will propose Discovery instead. See how we sell fixed-fee phased engagements.

ROI calculator — build a defensible business case in 7 steps

- 1Baseline current wait-time and abandonment. Pull 12 weeks of branch footfall, average and peak wait, walk-out rate. Most Kuwait banks see a 14-22 minute average wait on Sundays and salary week, with a 5-9% walk-out rate.

- 2Quantify teller-floor reallocation. A kiosk programme that moves 30-40% of routine cash and statement traffic off the teller floor frees teller hours for upsell and AML-sensitive work. Multiply hours saved per branch per week by fully-loaded teller cost.

- 3Quantify the appointment uplift. A mortgage, SME, or wealth appointment that closes is worth thousands of dinars in lifetime revenue. A 10-15% uplift in appointments-kept attributable to the new platform is realistic.

- 4Quantify complaint and NPS movement. A live customer-feedback loop tied to the queue ticket reduces complaint volume by 20-35% in our deployments. Price each complaint at handling cost (£40-£80).

- 5Quantify regulatory cost-avoidance. A CITRA breach or a CBK adverse finding is multiples of the platform cost. Sovereign on-prem reduces this risk; price the avoided cost in.

- 6Quantify brand cost. Kuwait is a small market with high social-media velocity. A viral complaint about a queue at a flagship branch reaches the executive committee inside a day. Price brand cost as 5-10% of marketing budget at risk.

- 7Sum, divide by Build cost, present payback in months. Most Kuwait bank programmes pay back inside 14-22 months on the Build phase alone.

Use this in the board paper. Add the Kuwait National Bank London case study as a reference annex.

Seven failure modes from Kuwait bank deployments

We have audited or recovered queue programmes at banks across the GCC. The same seven failures recur.

1. The English-first build with Arabic bolted on. Half-mirrored screens, broken kiosk layouts, ticket text overflowing. Fix: insist on EN+AR full-RTL bilingual baseline on day one.

2. The public-cloud SaaS that survives CIO review and then fails the CISO. The CIO is impressed by the demo; the CISO opens the data-flow diagram and the deal stalls for nine months. Fix: scope sovereign on-prem from Discovery.

3. The core-banking integration that was "included". Contract says "core-banking integration included"; the fine print only ships a webhook. The actual Temenos, Finacle, or Mambu adapter is a £60k change order. Fix: line-item every integration in Discovery.

4. The kiosk hardware vendor lock. The platform only works with one vendor's hardware, end-of-life next year. Fix: choose a platform that runs on commodity hardware and treats Ingenico, PAX, Verifone, and any printer brand as interchangeable.

5. The reporting that lives outside the bank. Reports are generated in the vendor's cloud and emailed to the bank. The CBK auditor asks "where does this data go?" and the answer is awkward. Fix: reporting inside the perimeter.

6. The exit you cannot execute. No exit clause, or a vague one. Three years later the bank wants to switch and the data export is undocumented. Fix: codified 90-day exit window on day one.

7. The change-orders that ate the budget. Build started at £180k and finished at £420k because the vendor priced thin and made margin on changes. Fix: fixed-fee Build with priced change-order menu and weekly demos.

The worldwide banking transformation guide catalogues the same failures across UK, EU, Americas, and Asia deployments.

Migration path — moving off a legacy ticket dispenser without breaking the branch

Most Kuwait banks already have a queue system: typically a generic ticket dispenser plus a static LED display. Migration to a regulator-aligned platform happens over six phases in 16-24 weeks for a mid-size network, without service interruption.

Phase 1 — Discovery (3-4 weeks). Branch-by-branch as-is mapping, stakeholder workshops with branch network, CIO, CISO, retail experience, and Vision 2035 lead. Output: regulator-aligned spec, fixed-fee Build scope, transition plan.

Phase 2 — Pilot branch (4-6 weeks). New platform in one flagship branch with the legacy system in parallel for two weeks. Measure wait-time, abandonment, NPS, teller-floor reallocation. Iterate twice.

Phase 3 — First wave rollout (4-6 weeks). Roll out to 5-10 branches in a region. Tune routing logic per service type with branch managers' input.

Phase 4 — Appointment + virtual queue overlay (2-4 weeks). Layer in the online appointment system and the virtual queue channel for mobile and WhatsApp joins. Most banks see a 20-30% reduction in lobby congestion within four weeks.

Phase 5 — Full rollout (4-8 weeks). Roll out region by region. Keep one branch per region on the old system as fallback. Decommission only after the new platform has run clean for 30 days.

Phase 6 — Exit-ready handover (2 weeks). Hand runbooks, repo, license keys, and operator training to the bank. The 90-day exit window begins the day the last branch is live.

This migration shape is what we have shipped at the Kuwait-branded bank in London and at adjacent state-bank engagements such as the Aljanoob Bank programme.

Implementation playbook — week-by-week of a 20-branch Kuwait bank rollout

For a 20-branch network from Discovery to full coverage in a calendar year:

- Weeks 1-3 — Discovery. Branch-by-branch as-is, stakeholder workshops, regulator-aligned spec.

- Weeks 4-6 — Build kickoff. Architecture sign-off, hardware procurement, core-banking integration design with the Temenos, Finacle, or Mambu team. OIDC is the default for staff-side SSO.

- Weeks 7-12 — Platform Build. EN+AR baseline, kiosk UX, signage templates, agent console, customer feedback integration, visitor management for staff-side check-in, digital signage creative.

- Weeks 13-16 — Pilot branch. One flagship, parallel-run with legacy, two-week measurement, iterate twice.

- Weeks 17-22 — First wave (5 branches). Region 1 rollout, daily stand-up, weekly executive review.

- Weeks 23-28 — Appointment + virtual queue overlay. Mobile and WhatsApp join, appointment booking for mortgage, SME, wealth.

- Weeks 29-40 — Full rollout. Three regions, 4-6 branches per fortnight.

- Weeks 41-44 — Stabilisation. 30-day monitoring, legacy decommission.

- Weeks 45-48 — Exit-ready handover. Runbooks, repo, training, opening of the 90-day exit window.

The entire programme runs fixed-fee, milestone-paid, with weekly demos to the branch network director and CIO.

Frequently asked questions

Does the queue platform need to integrate with the Kuwait national identity gateway?

Conditional. A walk-in customer drawing a ticket does not need full national-identity verification to take a number. A customer opening an account or running a KYC-sensitive transaction does, and that integration is handled at the teller or relationship-manager console rather than at the kiosk. The platform captures minimum necessary identity at the kiosk and passes the full KYC flow downstream per CBK guidance. We design this case-by-case in Discovery.

How does the platform handle Arabic full RTL on signage, kiosk, and SMS in the same deployment?

The bilingual EN+AR baseline is mirrored on every surface from day one. The kiosk renders RTL natively, floor signage flips column order and reading direction in Arabic mode, ticket text prints in correct RTL, and SMS or WhatsApp notifications respect locale. The customer's chosen language at the kiosk is propagated through the entire turn, including the agent console.

What is the CBK and CITRA posture if customer data is processed in a cloud region outside Kuwait?

CITRA's Data Privacy Protection Regulation and CBK guidance both make cross-border transfer a regulated act, achievable but requiring explicit legal basis, data-subject notification, and additional contractual controls. Our default for the regulated identity-capture path is to avoid the question: run sovereign on-premises inside the bank's perimeter.

How does the platform support Kuwait Vision 2035 customer-experience metrics?

The analytics layer ships with a Vision 2035-aligned KPI pack: wait-time by branch and region, abandonment rate, complaint volume, NPS, appointment-kept rate, and digital-channel adoption (mobile, WhatsApp, kiosk share of total tickets). These feed the executive dashboard and export to PDF or CSV for board reporting and regulator submission.

Can we integrate the queue platform with our Temenos, Finacle, or Mambu core?

Yes. We have shipped integrations to all three. The pattern is a thin adapter at the queue platform exposing a stable interface and a connector module on the core-banking side that the bank's integration team owns post-handover. Card-present hardware (Ingenico, PAX, Verifone) is a separate integration path scoped in Discovery. OIDC is the default for staff-side SSO.

Can the appointment system route a customer to a specific relationship manager?

Yes. The appointment system supports service-level, specialist, and named-person routing. A wealth client booking a portfolio review is matched to their named relationship manager; an SME booking a credit conversation is matched to the regional SME specialist available that day. The branch is selected by the customer; the staff member is selected by the rule.

How does the kiosk strategy interact with the teller floor?

A well-designed self-service kiosk takes 30-50% of routine traffic off the teller floor in a Kuwait branch. Cash deposit, cheque deposit, balance enquiry, statement print, card issuance, and PIN reset are typical kiosk-eligible services. The branch-floor design needs to signpost the kiosk path clearly; the queue platform routes kiosk-eligible services to the kiosk first and escalates to a teller on demand.

What does the 90-day exit window actually deliver?

The 90-day exit window is a contractual commitment that on contract end the bank receives: a documented data export in agreed format; a runbook covering platform operation, upgrade, and disaster recovery; license keys; repository transfer where the bank owns the source; and 90 days of supplier support while the operator's team takes over. Zeour treats this as default. It is what makes the engagement defensible to procurement: the bank is buying a platform it can run itself, not a captive subscription.

How do you handle KYC and AML rules during walk-in ticket capture?

The kiosk captures only what CBK guidance allows at first touch. Full KYC and AML checks happen at the teller or relationship-manager console where the regulated identity flow already lives. The queue platform attaches the chosen service to the right downstream KYC path; it does not perform KYC itself. This separation keeps the platform out of regulated identity-capture scope and simplifies the CITRA conversation.

Can we run a 4-week pilot before signing the full Build contract?

We prefer Discovery before any Build commitment. Discovery is fixed-fee, 3-4 weeks, and produces the spec the Build is priced against. A 4-week working-system pilot post-Discovery is achievable for a single-branch deployment in the £30k-£60k range and is the right step for a CIO who needs to see the platform live before a network-wide Build. Start with a conversation.

Where Zeour fits

Zeour Ltd is a UK-registered engineering firm shipping enterprise systems worldwide. Our queue management ecosystem is in production across 1,247+ branches in 40+ countries, including a Kuwait-branded private bank in London (see the case study). We deliver in fixed-fee phased engagements with a contractual 90-day exit window, so the operator owns the platform, the data, and the runbooks at the end.

We are not a public-cloud SaaS vendor. We deploy sovereign on-premises by default inside the bank's perimeter, because that is the cleanest answer to CBK and CITRA. We ship the bilingual EN+AR baseline as the production default for every GCC engagement. And we run on-premises AI where the bank wants conversational triage, complaint summarisation, or branch-manager assistants — open-weight models on the bank's own hardware.

If you are a CBK-supervised bank scoping a 2026 programme, the next step is Discovery. Fixed-fee, 3-4 weeks. Start a conversation or browse the /industries/banking playbook. For regional context, the KSA banks and worldwide banking transformation guides are companion reads.

---

This guide is part of Zeour's banking-industry buyer's-guide series. For cross-region context and the full enterprise queue management platform spec, browse the /industries/banking hub and the /pricing page.