Key takeaways

- UAE branches in 2026 sit inside a tighter perimeter: CBUAE customer-protection rules, the UAE Federal Data Protection Law (Federal Decree-Law 45/2021), TDRA telecom rules and the DIFC and ADGM regimes all shape how a queue management system handles personal data and waiting-time disclosures.

- A modern programme is a full customer-flow stack: pre-arrival booking, virtual queue, self-service triage, signage, feedback capture and analytics — bilingual EN+AR with full RTL by default.

- Sovereign deployment inside the bank's perimeter, or a UAE-resident sovereign cloud, is the default posture.

- Integration with core banking — Temenos, Finacle or Mambu — and with the federal digital ID and national identity gateway is where most programmes succeed or fail. Spec it before signing.

- We the UAE 2031 and UAE Centennial 2071 push banks toward measurable CX KPIs (NPS, waiting time, abandonment) that the QMS must report by branch and emirate.

- Budgets: Discovery £15k-£40k; small-footprint Build £100k-£350k; enterprise Build £400k-£1.5M; integrations £25k-£80k each; per-branch hardware £8k-£25k.

- Zeour ships the same QMS platform across 40+ countries. UAE programmes are one variant of a worldwide-deployed product, not a bespoke build.

If you run a UAE branch network in 2026, the QMS decision is no longer about hardware. It is a regulated, bilingual, identity-aware customer-flow programme.

Who this guide is for

This guide is written for four specific decision-makers in UAE banking:

- UAE bank branch network director running 50-300 branches across the seven emirates. You are accountable for waiting time, abandonment and cost per served customer, and you need one view across Dubai, Abu Dhabi, Sharjah, Ajman, Umm Al Quwain, Ras Al Khaimah and Fujairah without seven silos.

- CIO at a federal bank under CBUAE supervision. You carry the residency burden under the Federal Data Protection Law and need a QMS that runs on infrastructure you control, integrates with Temenos, Finacle or Mambu, and produces evidence on demand.

- Head of retail experience. You own NPS and the brand impression at the door. You need virtual queueing, pre-booked online appointments and a self-service kiosk that all carry your brand language.

- Programme director for We the UAE 2031 banking modernisation. You run a multi-year transformation tied to national-vision KPIs. You need defensible cross-emirate metrics, federal digital ID flows, and a platform that ages out gracefully without vendor lock.

If you sit outside these four roles you can still use the framework, but the rubric, cost bands and failure modes are calibrated to a CBUAE-supervised retail or commercial bank.

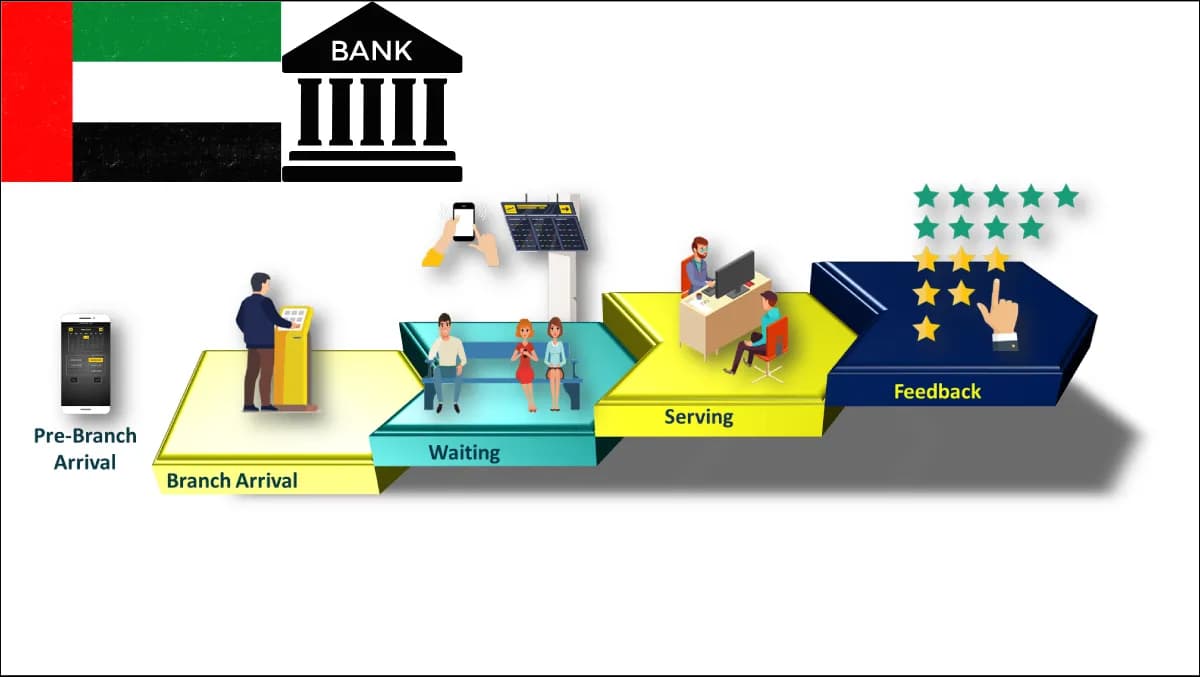

What is queue management in 2026 — and why it's different for the UAE?

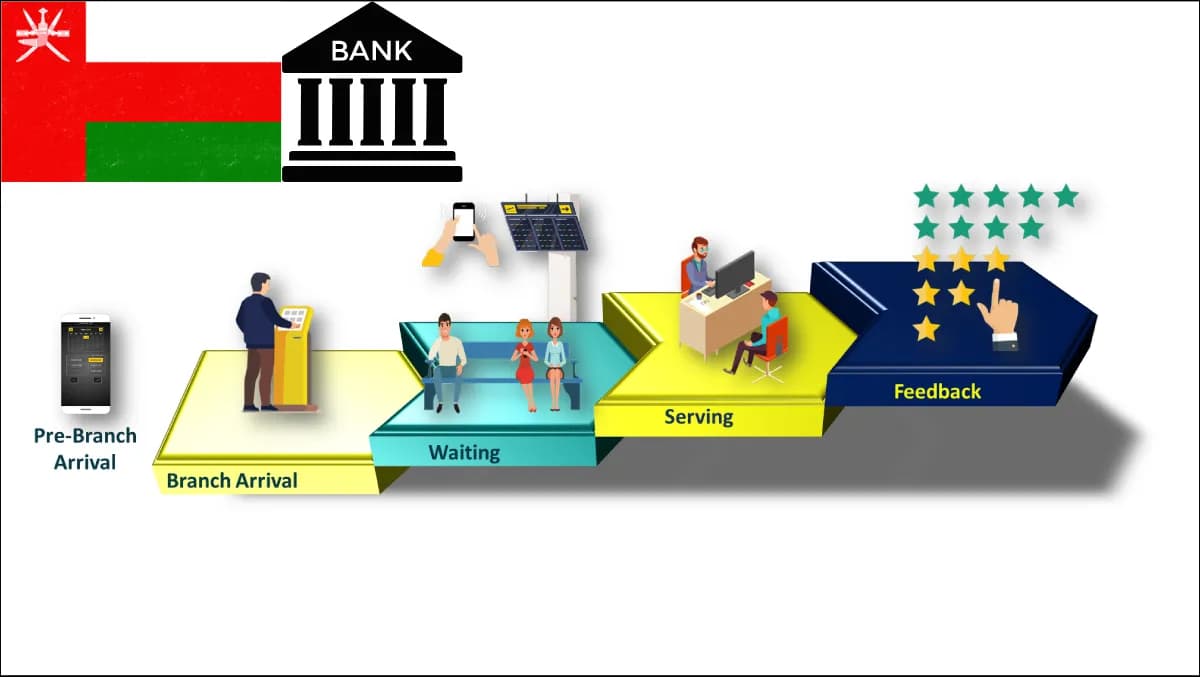

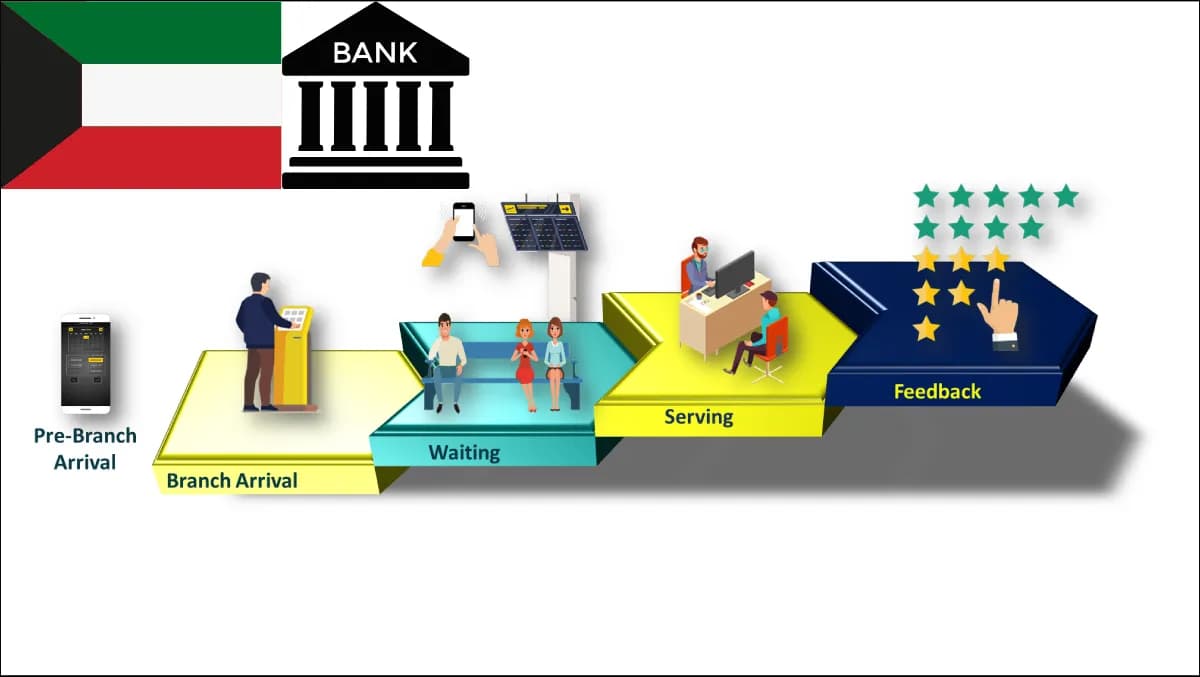

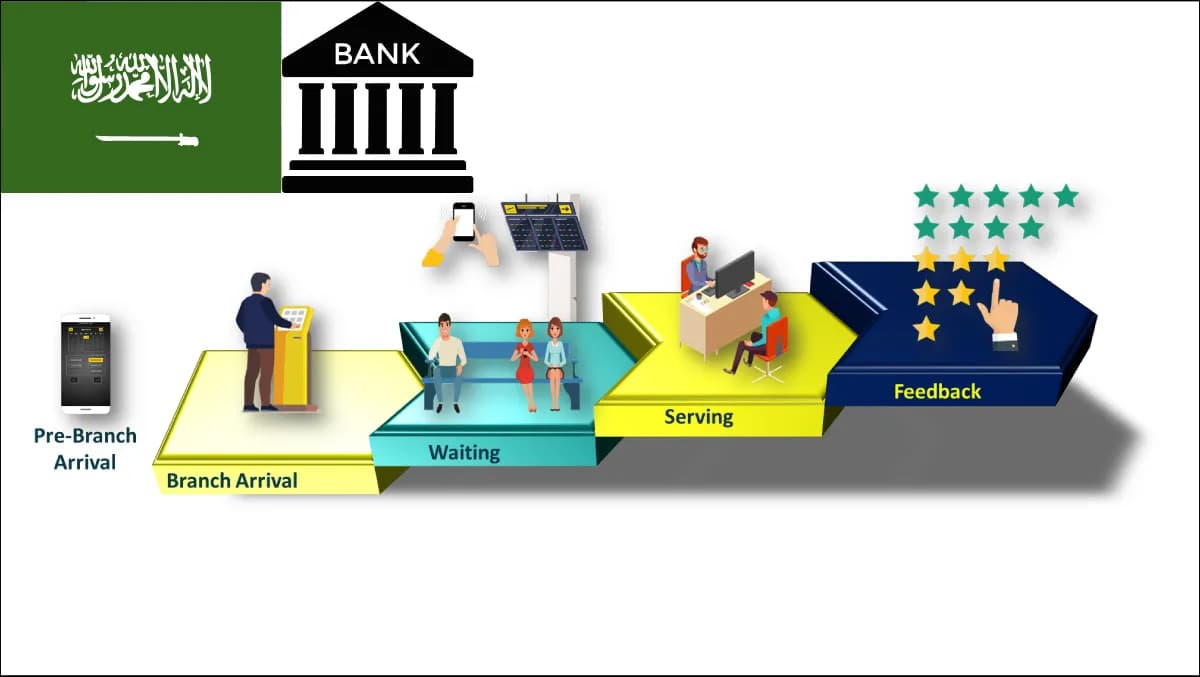

In 2026 a UAE bank QMS is no longer a ticket dispenser. It is the customer-flow control plane for the branch network. A modern deployment spans:

- Pre-arrival: web and mobile booking through an online appointment system, with slots tied to advisor skills and branches.

- Virtual queue: customers join from anywhere, see position in real time, and arrive five minutes before their turn. See our virtual queue management system.

- At the door: a bilingual self-service kiosk that triages purpose-of-visit, verifies the federal digital ID, issues a ticket and routes to the right counter group.

- In the branch: digital signage showing now-serving in Arabic and English, plus orchestration screens. A visitor management system handles vendor and contractor flows into back-office areas.

- At the counter: a teller interface tied into Temenos, Finacle or Mambu so the customer record is preloaded.

- After: a customer feedback system capturing the visit experience and feeding NPS and CBUAE metrics back into operations.

Three things make the UAE distinctive in 2026.

First, the regulatory layering. CBUAE rules require banks to publish service standards and report on adherence. The Federal Data Protection Law (Federal Decree-Law 45/2021) governs personal data at federal level. Inside the DIFC, the DIFC Data Protection Law applies; inside the ADGM, the ADGM Data Protection Regulation applies. A QMS processing Emirates ID numbers, account references and biometric checks has to navigate all three depending on where each branch sits. TDRA governs the SMS, voice and web channels the QMS uses.

Second, the bilingual baseline. English plus Arabic with full right-to-left support is a production baseline in every UAE branch — not an add-on. Kiosk, signage, ticket, SMS, email, printed receipt, staff screen and audit report — all in both languages, with locale-aware number, date and currency formatting. See our bilingual baseline notes.

Third, the federal-and-emirate identity stack. UAE banks live on top of the federal national identity gateway and the federal digital ID platform. The QMS needs to verify identity at the kiosk, pre-populate the teller record, and capture identification metadata that satisfies KYC and AML rules under CBUAE supervision.

Layer in We the UAE 2031, UAE Centennial 2071 and emirate-level programmes like Dubai's 10X agenda and Abu Dhabi's 2030 Plan, and the QMS becomes part of national-vision reporting. Branch waiting time is not just an operations KPI — it feeds into customer-protection adherence and national CX benchmarks.

The UAE-fit scoring rubric — 14 criteria

Use this 14-criterion rubric during Discovery to score any QMS against UAE banking reality. Each criterion scores 0-3; total /42.

| # | Criterion | What good looks like in the UAE |

|---|---|---|

| 1 | CBUAE customer-protection reporting | Waiting time, served vs abandoned, by branch and emirate, on-demand |

| 2 | Federal Data Protection Law residency | All personal data resident in the UAE or in the bank's perimeter |

| 3 | DIFC + ADGM regimes | Configurable retention and access per legal entity / free zone |

| 4 | Bilingual EN+AR with full RTL | Every UI, notification and report — Arabic-first where appropriate |

| 5 | Federal digital ID integration | Native verify + pre-fill from the federal stack |

| 6 | National identity gateway | Read identification metadata to satisfy KYC + AML |

| 7 | Core-banking integration | Temenos, Finacle, Mambu — pre-built or documented patterns |

| 8 | Counter device interoperability | Ingenico, PAX, Verifone PED and receipt-printer support |

| 9 | Sovereign deployment posture | On-premises or UAE-resident sovereign cloud |

| 10 | Multi-emirate operations view | One pane of glass across all seven emirates, role-scoped |

| 11 | Virtual queue + appointment unification | One customer record across booking, virtual queue and walk-in |

| 12 | Customer-feedback loop | Branch-level NPS, CSAT and CBUAE-grade complaint capture |

| 13 | Accessibility (WCAG 2.2 AA) | Keyboard, screen reader, large text, audio prompts on kiosk |

| 14 | Fixed-fee engagement and exit window | Discovery and Build priced fixed; 90-day post-handover exit window |

Score each candidate. A serious UAE-ready platform scores 32+/42. Anything below 24 has architectural gaps that will surface during CBUAE supervisory review or a Federal Data Protection Law audit.

How do you choose between on-premises, sovereign cloud, and public-cloud SaaS in the UAE?

This is the most common architectural question we get from CBUAE-supervised banks in 2026. The honest answer depends on data sensitivity, integration depth and the bank's existing infrastructure posture.

On-premises — the QMS runs inside the bank's UAE data centres, on hardware the bank owns. Default for tier-one CBUAE-supervised banks. It maximises sovereignty and is the only model that lets the QMS sit on the same VLAN as Temenos, Finacle or Mambu without crossing a network boundary.

Sovereign cloud in the UAE — the QMS runs on a UAE-resident tenancy with data residency contractually guaranteed inside the UAE. Reasonable for mid-market banks. It trades some on-premises sovereignty for elastic capacity. CBUAE supervisory expectations accept this as long as residency and access controls are documented.

Public-cloud SaaS with cross-border data flow — rarely the right answer for a CBUAE-supervised bank handling Emirates ID numbers and KYC artifacts. Even when the SaaS vendor advertises a UAE region, the contractual posture is often weaker than sovereign-cloud or on-premises, and the supervisory burden increases.

Zeour ships in all three modes, but the UAE banking default is on-premises or UAE-resident sovereign cloud, with the bank holding the encryption keys and OS credentials. Our enterprise development services team handles the deployment topology in Discovery.

> CBUAE supervisory point of view. A QMS handles personal data, identification metadata and operational telemetry that CBUAE may request during a supervisory visit. If the data sits in a foreign jurisdiction under a foreign vendor's control, the burden of evidence is higher. On-premises or sovereign-UAE deployment resolves the supervisory question before it gets asked.

How much does a UAE bank QMS cost in 2026?

The honest answer depends on branch count, integration depth and emirate spread. Indicative bands in pound sterling; local-currency quotes are produced during Discovery:

- Discovery: £15k-£40k. Two to six weeks. Branch-flow profiling, integration mapping, data-residency posture and a fixed-fee Build statement of work. Bilingual EN+AR workshops included.

- Build, small footprint: £100k-£350k. One brand, 20-80 branches in 1-3 emirates. Core QMS, bilingual kiosks, signage, virtual queue, basic core-banking integration, on-premises in one data centre.

- Build, enterprise footprint: £400k-£1.5M. 100-300 branches across all seven emirates, multi-brand support, federal digital ID integration, full appointment + virtual-queue + walk-in journey, customer feedback, on-premises HA across two data centres.

- Integrations: £25k-£80k per system. Temenos, Finacle, Mambu, the national identity gateway, the federal digital ID, CRM and data warehouse each count as one. Most banks need 4-7.

- Per-branch hardware: £8k-£25k. Bilingual self-service kiosk, signage screens, ticket printer, counter-display unit, network gear. Higher for flagship branches; lower for community-banking branches.

- Run cost: typically 12-18% of Build per year, covering maintenance, upgrades, regulatory updates and remote support during UAE business hours.

A representative tier-one programme — 180 branches, federal digital ID and Temenos integration, on-premises across two UAE data centres — lands at £750k-£1.2M for Build, £1.8M-£3.5M for branch hardware, and £110k-£200k per year for run. Comparable in shape to our KSA banks guide; UAE programmes tend toward smaller branch counts with more emirate-level operational complexity.

ROI calculator — build a defensible business case in 7 steps

This is the seven-step calculation we recommend running in Discovery so the case is defensible to a CFO, a CBUAE auditor and a board investment committee.

- 1Baseline waiting-time cost. Measure current median and 95th-percentile waiting time per branch. Multiply by walk-in volume. Apply an abandonment rate — typically 6-14% of walk-ins leave without being served. Each abandoned customer is worth £40-£180 in deferred revenue depending on segment.

- 2Baseline staff cost. Count branch-floor manager hours spent on queue triage, ticket reprints and escalation. In a mid-sized branch this is 8-14 hours per week. Multiply by fully loaded cost per hour.

- 3Project the post-deployment baseline. A virtual-queue + appointment + kiosk deployment in our portfolio reduces median waiting time by 35-55% and abandonment by 40-60%. Use the conservative end (35% / 40%) for the business case.

- 4Value the recovered customers. Multiply recovered customers by segment value. Retail current-account: £40-£90; premier or business: £150-£400.

- 5Value the staff time recovered. Floor managers shift from triage to selling. Assume 4-7 hours per branch per week recovered.

- 6Value brand and complaint reduction. Branch-level NPS improvement of 8-18 points is typical. Customer-protection complaints to CBUAE drop by 25-45% in mature deployments. Quantify regulatory-cost avoidance.

- 7Subtract programme cost. Use Discovery + Build + run from the bands above. Payback is typically 14-24 months for enterprise deployments and 10-18 months for small-footprint. IRR over five years is typically 35-90%.

Document every assumption. The strongest business cases are the ones the CFO can re-run with their own numbers.

Seven failure modes from UAE deployments

Across deployments in the GCC and the broader worldwide banking portfolio, these seven failure modes are the most common reasons a UAE bank QMS programme stalls:

- 1The QMS is bought before integrations are scoped. The bank picks a vendor, signs, then discovers Temenos integration is a six-month custom build. Discovery should produce the integration spec before procurement closes.

- 2The bilingual journey is treated as a translation layer. Arabic is not English with substituted strings. RTL layout, number formats, date formats, name ordering, voice-prompt phrasing, audio-cue timing — all distinct. A platform that bolts Arabic on top of an English-first product fails the bilingual baseline test in branch.

- 3Free-zone data regimes are missed. A branch in the DIFC operates under DIFC Data Protection Law; a branch in the ADGM under ADGM Data Protection Regulation; everywhere else under the Federal Data Protection Law. Same platform, different retention rules, different data-subject rights. If the QMS cannot configure per legal entity, you have a compliance problem.

- 4Federal digital ID is treated as out-of-scope. Customers expect to verify identity at the kiosk with the federal digital ID. If the QMS does not integrate with the federal stack, the kiosk becomes a slow paper-form replacement and abandonment goes up.

- 5The reporting layer is generic. Generic dashboards do not satisfy CBUAE supervisory questions. A UAE-ready QMS reports waiting time, served vs abandoned, NPS, complaint volume and customer-protection adherence by branch and by emirate.

- 6Devices are over-customised at the door. Every branch wanting a different kiosk layout creates a fragmented estate that is impossible to operate at scale. Standardise per branch tier; allow configuration, not customisation.

- 7There is no exit window. A programme without a 90-day exit window and a documented handover plan locks the bank in. Zeour ships every programme with the repo, the deploy keys and the operating runbook to the bank at handover. Insist on this clause.

Migration path

Most UAE banks reading this are not greenfield. You have an existing QMS — typically a 7-12-year-old hardware-led platform. The migration path that has worked is four stages:

Stage 1: Parallel pilot in 3-6 branches across 2-3 emirates. Pick a mix of flagship, full-service and community branches. Run new and old QMS side by side for 8-12 weeks. This is where bilingual EN+AR is stress-tested.

Stage 2: Brand-by-brand or emirate-by-emirate rollout. Roll out 15-30 branches per month. Co-existence with the legacy QMS continues. Every floor manager needs 4-6 hours of bilingual training.

Stage 3: Integration deepening. Once the network is on the new platform, deepen the integrations — federal digital ID, core banking, CRM, data warehouse, customer-feedback loop. ROI moves from operational to strategic.

Stage 4: Decommission and handover. Retire the legacy QMS, hand over the repo, deploy keys and runbook to the bank, and start the 90-day exit window.

Most programmes take 9-18 months end to end. Programmes that rush stage 1 always pay for it later in stage 3 — invest in the parallel pilot.

Implementation playbook

A condensed playbook for a UAE bank QMS programme:

- Week 0-2: Mandate and sponsorship. A CBUAE-supervised programme needs sponsorship from the COO or head of retail, not just IT.

- Week 2-8: Discovery. Branch-flow profiling, integration mapping, bilingual UX workshops, data-residency decision, fixed-fee Build SOW. See our pricing page for indicative shape.

- Week 8-20: Pilot Build and deployment. Stand up the platform. Build pilot-branch integrations (core-banking and federal digital ID first). Deploy in 3-6 branches. Run for 8-12 weeks.

- Week 20-60: Rollout. Branch-by-branch, brand-by-brand or emirate-by-emirate. Weekly steering, bi-weekly metrics review.

- Week 60-72: Integration deepening + decommission. Retire the legacy QMS. Sign off the operational runbook.

- Week 72-84: Exit window. Bank operates independently with Zeour on-call. Repo, deploy keys, license keys and runbook handed over.

Two operating principles matter most throughout. First, measure relentlessly — branch-level waiting time, abandonment, NPS, complaints, staff time recovered, every week. Second, report transparently — to the CIO, COO, board, and CBUAE where requested.

For a reference deployment in a different jurisdiction, see the Kuwait National Bank London case study, which used the same platform. For a heavier-engineered customer-flow deployment, see Aljanoob Bank. For broader sector framing, see our banking branch transformation buyer's guide and the generic queue management system buyer's guide.

Frequently asked questions

Does a UAE bank QMS need to be physically deployed in the UAE?

For a CBUAE-supervised bank handling Emirates ID data and KYC artifacts, the practical answer is yes — either on-premises in the bank's UAE data centres or on a UAE-resident sovereign cloud tenancy with documented residency. Cross-border SaaS is rarely the right answer.

How does the QMS integrate with the federal digital ID and the national identity gateway?

Via documented patterns at the kiosk and appointment layer — typically OIDC-style flows. The QMS verifies the customer, pre-populates the teller record, and stores only what is legally necessary. The integration is a Discovery output.

Does it integrate with Temenos, Finacle and Mambu?

Yes. We have shipped integrations with all three across our banking portfolio. Each is scoped during Discovery and built fixed-fee. Integration typically lives at the customer-record-lookup layer, the product-eligibility layer and the post-visit telemetry layer.

What about Ingenico, PAX and Verifone PEDs at the counter?

Supported. The QMS does not replace the payment-terminal estate but interoperates with it where the bank needs combined receipts or unified ticketing. The common pattern is the PED at the counter with the QMS providing the ticketing, signage and bilingual customer-facing UI.

How does this fit We the UAE 2031 and UAE Centennial 2071?

We the UAE 2031 includes financial-sector modernisation and customer-experience targets that translate into branch-level KPIs. The QMS is the system of record for those KPIs and produces the reporting that lets the bank demonstrate adherence alongside CBUAE customer-protection standards.

How is bilingual EN+AR handled in practice?

Full RTL layout, Arabic-first where appropriate, locale-aware date and number formats, correct Arabic-numeral vs Western-numeral display per context, voice prompts in both languages, printed-receipt rendering with correct script. This is engineering work, not a translation pass.

What is the difference for branches in the DIFC and ADGM?

Branches in the DIFC fall under the DIFC Data Protection Law and the Dubai Financial Services Authority perimeter. Branches in the ADGM fall under the ADGM Data Protection Regulation and the Financial Services Regulatory Authority. The QMS must be configurable per legal entity so retention, access and data-subject-rights handling differ by free zone. Everywhere else, the Federal Data Protection Law applies.

What is the typical timeline from contract to first live branch?

For a small-footprint programme, 8-14 weeks from signed contract to first live branch. For an enterprise programme with deep integrations, 16-24 weeks. Discovery is 2-6 weeks; pilot Build runs in parallel.

How does TDRA affect the QMS?

TDRA regulates the telecommunications layer the QMS uses — SMS, voice notifications, web messaging. Practical implications include the SMS aggregator contract, notification format and consent posture for customer messaging. The Discovery output includes a TDRA-aligned messaging design.

What happens at the end of the engagement?

A 90-day exit window. At handover the bank takes the repo, deploy keys, license keys and operating runbook. Zeour remains on-call for 90 days. After the window the bank is fully self-sufficient, with the option of an ongoing Care Plan. This is contractual, not aspirational — see our fixed-fee engagement notes.

Where Zeour fits

Zeour Ltd is a UK-registered engineering firm operating the same QMS platform across more than 1,247 branches in 40+ countries. The UAE programme is one variant of a worldwide-deployed product. The failure modes above are ones we have already engineered around in other markets, and sovereign-deployment, engineered-multilingual and federal-identity-integration patterns are battle-tested.

The UAE-specific posture combines six anchors:

- 1Sovereign on-premises by default — the platform runs inside the bank's UAE data centres or a UAE-resident sovereign cloud tenancy, with the bank holding the encryption keys and OS credentials.

- 2Engineered multilingual — English and Arabic with full RTL ship as a production baseline. French, Urdu, Hindi and other languages spoken by UAE residents and visitors are added per engagement as a three-file configuration change.

- 3Production portfolio as proof — every product on the site is a real, deployed system, including reference deployments on our banking industry page and named case studies like Kuwait National Bank in London.

- 4Fixed-fee phased engagements — Discovery is fixed-fee; Build is milestone-fixed with weekly demos; change orders are explicit and priced. The bank knows the cost shape before signing.

- 5On-premises AI without giving up capability — open-weight LLMs running on the bank's hardware can power post-visit feedback analysis, branch-level anomaly detection, and bilingual complaint triage without sending personal data to a foreign cloud.

- 6Worldwide reach with regional strength in the GCC and MENA — direct delivery from London across the UAE, supported by certified partners in the region.

If you are scoping a UAE bank QMS programme for 2026, the next step is a Discovery conversation. We will walk the candidate branches, map your integrations, draft the data-residency posture and produce a fixed-fee Build statement of work. Contact our engineering team to start.

---

Related reading: queue management for KSA banks, banking branch transformation buyer's guide, queue management system buyer's guide, banking industry page.