Key takeaways

- The Central Bank of Oman (CBO) is the prudential anchor for any branch technology decision in 2026 — your queue management system is part of the customer-data and channel surface that CBO supervises, and its cybersecurity framework now applies end to end.

- The Oman Personal Data Protection Law issued under Sultani Decree 6/2022 binds you to data-minimisation, lawful basis, breach notification and cross-border transfer discipline — your QMS handles personal data at the ticket, the appointment, the kiosk, and the feedback prompt, so the sovereign deployment posture is no longer a stylistic choice.

- Oman Vision 2040 and MTCIT's e-government direction reward in-country processing, accessible bilingual UX, and operator self-sufficiency. A vendor that holds your data hostage in a foreign region will eventually be the procurement risk that pulls a programme off track.

- A defensible programme buys three things at once — an on-premises queue management core, a virtual queue layer reachable by SMS and WhatsApp, and an online appointment channel that the core banking system can trust — not three loosely coupled tools.

- Expect Build pricing in the £80k-£220k band for small to mid-sized Omani banks (15-40 branches under one brand) and £300k-£900k for an enterprise rollout (50-80 branches with multiple lines of business, branches outside Muscat, and Temenos / Finacle / Mambu integration).

- A bilingual baseline of English and Arabic with full RTL is mandatory at every surface — ticket, kiosk, signage, host screen, mobile, receipt, audit log. Anything bolted on later as a translation layer fails CBO and PDPL scrutiny.

- Buy with a fixed-fee engagement and an explicit 90-day exit window. Operator self-sufficiency at exit is the only credible defence against vendor lock-in in a market this size.

Oman is a smaller, more concentrated banking market than its GCC peers — fewer banks, fewer branches, and a customer base that expects the same digital polish as the wider Gulf without the same procurement margin for error. The branch is still where home loans, SME onboarding, expat remittances, government salary accounts, and high-value retail conversations happen — and it is where CBO, MTCIT, and TRA can each look you in the eye on data residency, accessibility, and cybersecurity. This guide is the senior engineer's view of how to buy QMS for an Omani bank in 2026.

Who this guide is for

Four personas routinely sit in the same room when an Omani bank approves a QMS programme. Each reads the same RFP differently.

The branch network director running 15-80 branches across Muscat, Sohar, Salalah, Nizwa, and the interior cares about average teller-to-customer time, abandonment, and the cost of putting any new device on a counter. They have lived through earlier queue systems that did not survive a branch refurbishment cycle.

The CIO under CBO supervision owns the regulatory exposure. They read the brief through the CBO cybersecurity framework, data-residency under PDPL, and the integration risk of touching Temenos, Finacle, or Mambu core banking. They want a single-tenant deployment they can audit.

The head of retail experience is judged on Net Promoter Score and how the bilingual experience reads to an Arabic-first customer at a regional branch versus a bilingual professional in Muscat. They want the customer feedback loop closed at the same kiosk that issued the ticket.

The Vision 2040 transformation programme lead is steering a multi-year plan to digitise the branch network and integrate it with national digital identity and the e-government rails set by MTCIT and TRA. They need a vendor whose roadmap they can co-author.

If any of those four roles signs off on your QMS, the next sections are written for you.

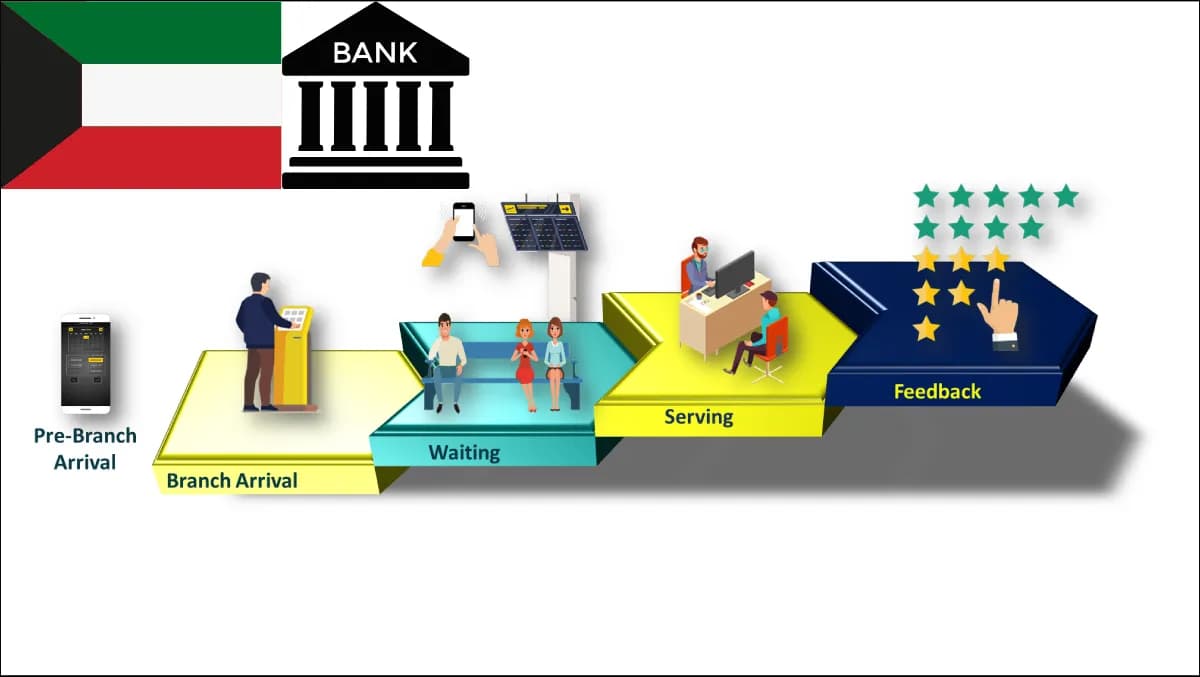

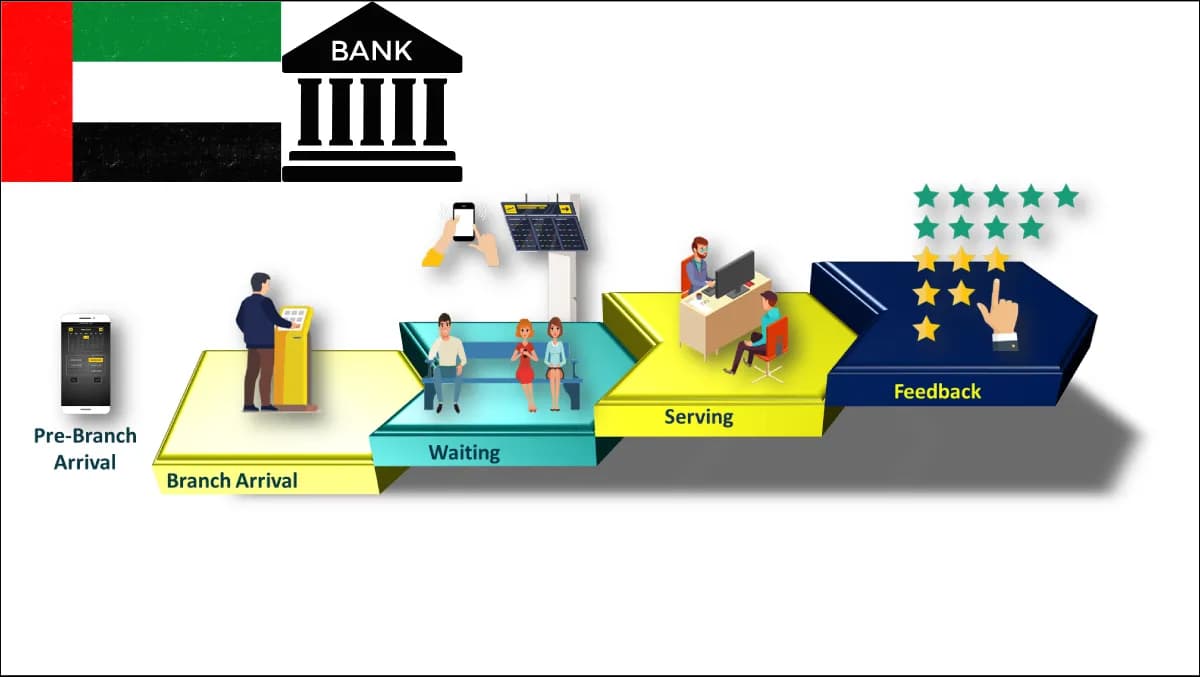

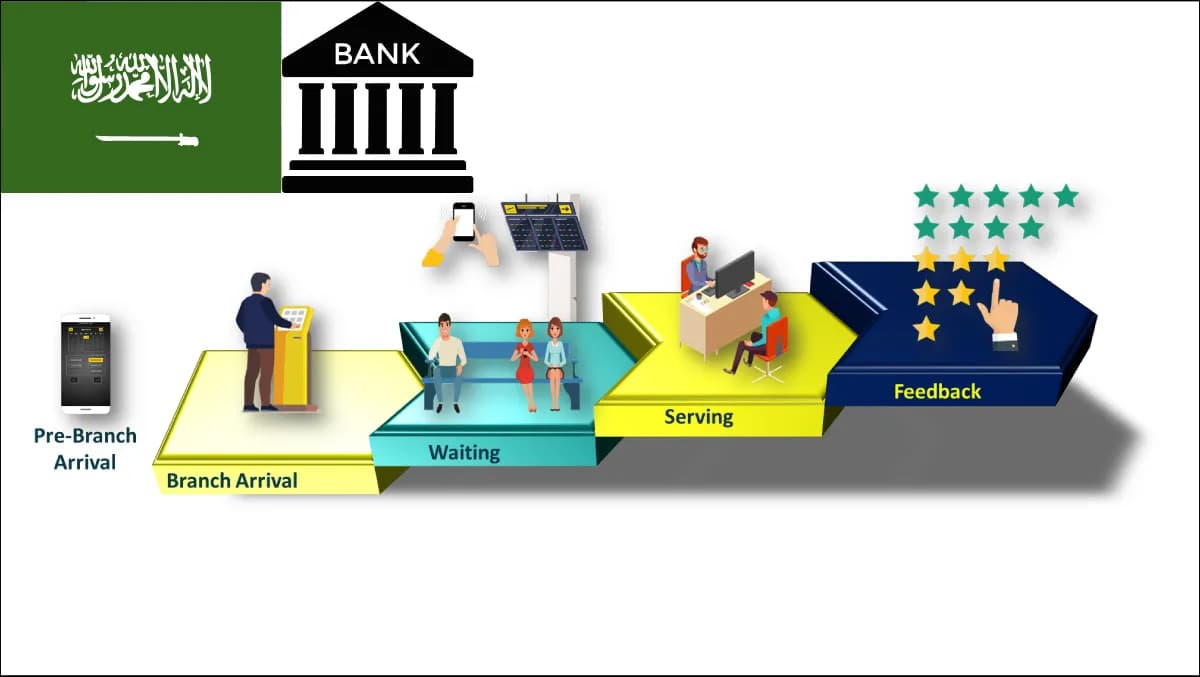

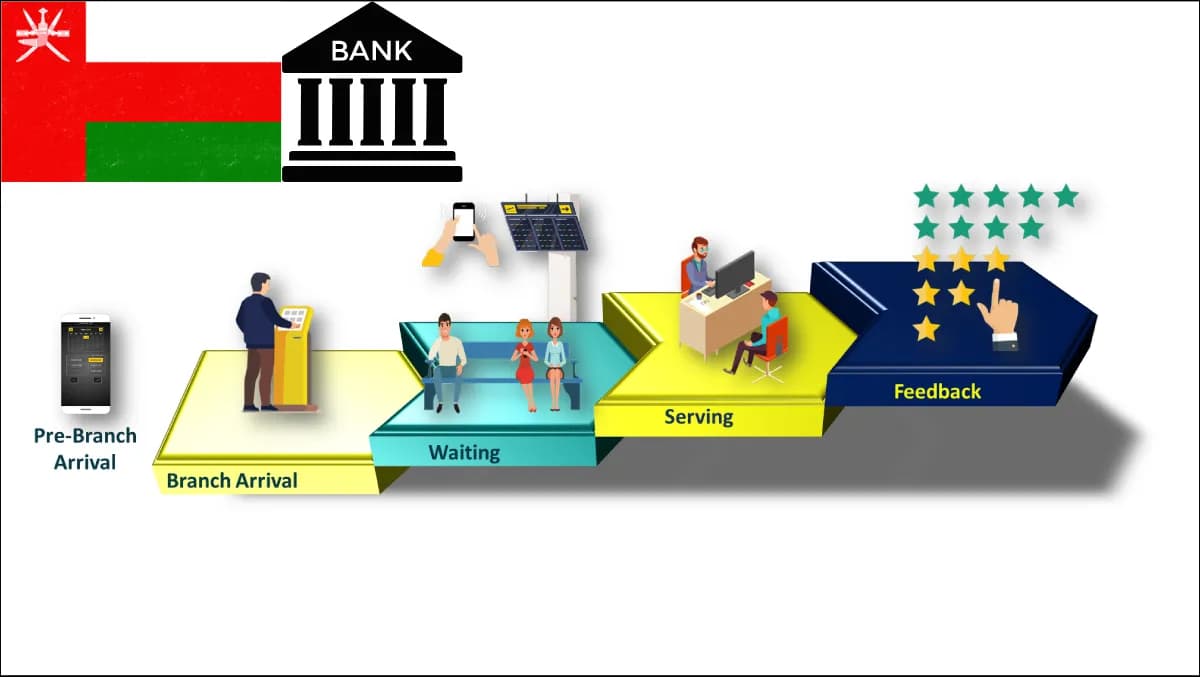

What is queue management in 2026 — and why it is different for Oman?

Queue management in a 2026 bank is no longer the ticket dispenser at the door. It is a small distributed system that runs at the branch and at the centre — and in Oman it is shaped by four forces at once.

First, CBO is steadily tightening expectations on operational resilience and cybersecurity. Branch-side infrastructure that touches customer identifiers or transaction context now sits inside that perimeter. A QMS that exfiltrates personal data to an offshore region is harder to defend each year than the year before.

Second, Sultani Decree 6/2022 has moved Oman onto a recognisable GCC PDPL footing — lawful basis, data minimisation, subject rights, breach notification, controller-processor discipline, and restrictions on cross-border transfers. Your QMS captures phone numbers at the virtual queue, national IDs at the self-service kiosk, visit logs through the visitor management flow, and free-text feedback. All of it is regulated personal data.

Third, TRA and MTCIT are nudging the country toward sovereign-by-default digital infrastructure. The national identity gateway, the unified citizen-services portal, and the e-government bus prefer in-country processing and well-audited integrations. A bank QMS that fits cleanly into that picture earns regulatory and reputational credit.

Fourth, Oman Vision 2040 frames the operational ambition. Branch digitalisation, accessibility, and bilingual service quality are markers of how a regulated industry is moving with the country. A QMS shipping a bilingual baseline of English and Arabic with full RTL across every screen is the floor.

Put together, the 2026 QMS has to be three things at once — a real-time branch OS, a sovereign data store under PDPL discipline, and a citizen-grade bilingual UX. Most platforms sold into Oman were not designed for all three.

The Oman-fit scoring rubric — 14 criteria

Use this as the scoring sheet inside your evaluation committee. Each row is binary or banded; weight by your own programme.

| # | Criterion | What good looks like in Oman 2026 |

|---|---|---|

| 1 | CBO cybersecurity alignment | Documented controls map to CBO framework; pen-test report ≤ 12 months old |

| 2 | PDPL data residency | All personal data stored and processed inside Oman; cross-border transfer only with lawful basis |

| 3 | Sovereign on-premises option | Single-tenant on-premises or in-country private cloud, not multi-tenant offshore SaaS |

| 4 | Bilingual EN+AR full RTL | Every surface — ticket, kiosk, signage, host screen, mobile, receipt, audit log |

| 5 | Core banking integration | Temenos, Finacle, Mambu adaptors as production references, not slideware |

| 6 | Identity gateway pattern | Ready to consume the national identity gateway via OIDC when made available to the bank |

| 7 | Payments terminal integration | Ingenico, PAX, Verifone EMV terminals at counter and kiosk where cash and card meet |

| 8 | Accessibility | WCAG 2.2 AA; large-print ticket; audio prompts; wheelchair-height kiosk variants |

| 9 | Branch resilience | Branch keeps serving offline; reconciles cleanly when the link returns |

| 10 | Real-time analytics | Sub-second branch metrics; daily and monthly retention configurable per PDPL |

| 11 | Appointment + virtual queue parity | Same identity, ticket, and SLA whether the customer walks in, calls, or uses online appointment |

| 12 | Feedback at the moment of truth | Customer feedback prompt at counter or kiosk before the customer leaves |

| 13 | Vendor portfolio proof | Production deployments at banks under CBO-equivalent regulators across the region |

| 14 | Fixed-fee + 90-day exit | Fixed-fee engagement; operator owns the repo, license, and deploy keys at exit |

If a vendor cannot show production evidence on rows 1, 2, 3, 4, and 14, the conversation should end there. Those five are the floor in an Omani CBO-supervised programme.

How do you choose between on-premises, sovereign cloud, and public-cloud SaaS in Oman?

The decision is shaped by Sultani Decree 6/2022 and the CBO cybersecurity framework more than by any single technical preference.

On-premises at the branch and the data centre is the highest-control posture. Personal data never leaves the bank's perimeter; you own the keys; CBO audit access is direct; PDPL data-residency is trivially satisfied. The trade-off is operational discipline — patching, monitoring, capacity, DR. For most Omani banks with an established IT operations function, that is a known cost. This is the posture Zeour ships by default and the one the Oman government-bank case study is built on.

Sovereign cloud inside Oman — single-tenant tenancy with an in-country provider — is a credible middle path when the bank does not want to operate a second data centre but is unwilling to risk offshore processing. It keeps PDPL residency clean and CBO audit posture defensible.

Public-cloud SaaS in an offshore region is easiest to procure and hardest to defend. Cross-border transfer restrictions under PDPL, CBO scrutiny on customer-data processors, and the multi-tenant blast-radius problem usually disqualify it for the regulated workloads. It may still have a place for non-personal analytics — not for the QMS core.

A defensible 2026 architecture in Oman is on-premises or sovereign cloud for the regulated core, with non-regulated tooling wherever is most economical.

> Call-out — three numbers anchor any CBO-facing business case: average teller-to-customer time today, abandonment rate at the 11:00-13:30 peak, and the share of branch visits that could have been an appointment or virtual queue. Walk in with those three; everything else follows.

How much does queue management cost in Oman in 2026?

Omani QMS programmes typically quote in Omani Rial during Discovery and contract in OMR with reference-rate clauses for imported hardware. Ranges below are in £ for budgeting clarity.

| Phase | Small bank (15-40 branches) | Enterprise bank (50-80 branches, multiple LOBs) |

|---|---|---|

| Discovery | £15k-£40k | £25k-£60k |

| Build | £80k-£220k | £300k-£900k |

| Core banking + payments integration | £25k-£70k per system | £40k-£150k per system |

| Hardware (per branch) | £8k-£18k | £12k-£25k |

| Care plan (annual) | £15k-£45k | £45k-£140k |

Three drivers move you within the band.

Branch profile. A regional branch with two tellers has a different hardware bill than a Muscat flagship with separate retail, business, and wealth zones. A blended per-branch estimate is honest; a single fixed figure is not.

Integration scope. A Temenos or Finacle integration that goes beyond CIF lookup into account-status, hold-balance, and AML flag pulls into the upper band. Mambu integrations on greenfield digital-banking units land lower because the API surface is modern.

Bilingual depth. A bilingual baseline properly delivered at every screen, receipt, signage panel, and audit-log entry is engineering, not translation. Cutting corners costs more later when CBO or an internal auditor flags an English-only screen.

For a worked range against your own footprint, see pricing or open a conversation via contact.

ROI calculator — build a defensible business case in 7 steps

The CBO-facing investment committee will not approve a QMS programme on customer-experience adjectives. It will approve a number. Build it in seven steps.

- 1Baseline the wait. Measure current average teller-to-customer time across a representative two-week window, branch by branch.

- 2Quantify abandonment. Count customers who join the queue and leave before being served, especially at 11:00-13:30. Translate to lost account-opening, mortgage enquiry, and SME walk-in volume.

- 3Cost the teller minute. Fully-loaded teller cost per minute multiplied by minutes saved at scale is the productivity line.

- 4Cost the branch square metre. Smaller queues shrink the lobby footprint required. In Muscat retail rates, that is a real number.

- 5Cost the avoidable branch visit. Visits that should have been an online appointment or a virtual queue handover are pure cost.

- 6Cost the regulatory tail. A PDPL incident at a QMS that mishandled personal data is not theoretical. Budget the credible downside.

- 7Sum and discount. Three-year NPV at the bank's hurdle rate. Payback inside 18 months on conservative assumptions deserves approval.

The deeper banking branch transformation playbook walks this through with worked numbers; the structure here fits one slide in an Omani board pack.

Seven failure modes from Oman deployments

Failures in Omani programmes cluster in predictable ways. Avoid all seven and the programme is mostly mechanical.

- 1Translation as afterthought. A vendor demonstrates English UX in the pitch and promises Arabic later. The bilingual baseline is a foundation, not a feature.

- 2Offshore SaaS with a local proxy. A multi-tenant SaaS with a Muscat sales presence is still a multi-tenant SaaS; CBO and PDPL do not care about the address on the business card.

- 3Core integration discovered late. Temenos or Finacle integration scope misunderstood until UAT. The cost line moves; the deadline slips; trust erodes.

- 4Hardware procurement chaos. Counter displays, kiosks, and ticket printers ordered piecemeal across three suppliers with no spare-parts plan. Branch downtime within the first year is then a question of when, not if.

- 5Bilingual receipts forgotten. The kiosk screen is bilingual; the receipt is English-only. Auditors notice.

- 6No closed feedback loop. Customer leaves the branch unhappy; the customer feedback prompt does not exist; the bank learns six weeks later from social media.

- 7No exit plan. Year three: vendor wants a price increase; bank has no source code, no deploy keys, no documentation. The exit window prevents this from becoming a multi-million-rial problem.

Every one of these is a contract or architecture decision, not a technology accident.

Migration path

Most Omani banks doing a QMS refresh in 2026 are not greenfield. They are replacing an older queue system that has aged out of support, lost its Arabic depth, or failed a CBO or internal-audit observation. The migration path has shape.

Phase 1 — parallel pilot at two contrasting branches. Pick one flagship Muscat branch and one regional branch. Run the new QMS alongside the legacy for four to six weeks. Treat the regional branch as the harder test — connectivity, hardware refresh cycle, and bilingual reading patterns all stress the system differently.

Phase 2 — controlled rollout in waves of 5-10 branches. Each wave gets a fixed-fee scope; each wave has a stop-the-line authority for branch operations.

Phase 3 — decommission the legacy. The legacy QMS comes off the network only when the new system has been in production for at least one CBO reporting cycle on every branch in scope.

Phase 4 — extend. Virtual queue, online appointment, digital signage, feedback, and visitor management for premium and SME zones come on once the foundation is steady.

The sibling GCC posts on KSA banks, UAE banks, and Kuwait banks describe the same shape adapted to each jurisdiction — proof that the pattern travels.

Implementation playbook

The playbook below has worked across multiple Omani-style programmes. Adapt; do not skip.

Weeks 1-4 — Discovery, fixed-fee. Branch profile audit; CBO cybersecurity control mapping; PDPL data-flow map; bilingual UX walkthrough; Temenos / Finacle / Mambu integration audit; current-state metrics baseline.

Weeks 5-12 — Architecture and build phase 1. On-premises or sovereign-cloud target architecture; OIDC pattern for the future national-identity gateway; payments-terminal integration with Ingenico, PAX, or Verifone; bilingual screen, ticket, kiosk, and receipt design.

Weeks 13-18 — Pilot two branches. Parallel-run; collect metrics; iterate.

Weeks 19-32 — Wave rollout. 5-10 branches per wave; stop-the-line authority with branch ops.

Weeks 33-40 — Extend channels. Virtual queue via SMS and WhatsApp; appointment booking from the bank's mobile and web; digital signage in lobbies; feedback at counter and kiosk.

Weeks 41-48 — Optimise and prepare for hand-over. Real-time analytics review; PDPL retention policy verification; AR receipt and audit-log review; rehearsal of the exit window hand-over so it is real, not theoretical.

For the same playbook walked through against your own branch network, contact is the route in.

Frequently asked questions

Does the Central Bank of Oman approve specific QMS products?

CBO does not certify QMS products; CBO supervises banks. Any system inside the bank — including the branch queue management and visitor management stack — sits inside the bank's documented cybersecurity, data-protection, and operational-resilience controls. The procurement question is not "is this vendor certified" but "can we defend this architecture in our next CBO review".

How does Sultani Decree 6/2022 affect a QMS purchase?

The Oman Personal Data Protection Law requires lawful basis, data minimisation, subject rights, breach notification, and discipline around cross-border transfers. A QMS captures phone numbers, national IDs, visit logs, and free-text feedback — all regulated personal data. The implication is that the QMS should run in a sovereign deployment posture with retention policies, audit trails, and consent capture aligned to PDPL from day one, not retrofitted.

Is on-premises really necessary, or will sovereign cloud do?

Either can satisfy PDPL data residency and CBO operational expectations, provided the cloud is single-tenant and in-country. Banks already operating data centres usually find on-premises the lower marginal cost and cleaner audit story; banks consolidating away from physical infrastructure may prefer in-country sovereign cloud. Offshore multi-tenant SaaS is the option that struggles to defend itself.

What does bilingual EN+AR full RTL actually mean for an Omani branch?

Every surface that a customer or operator sees renders correctly in both languages with full right-to-left layout — tickets, kiosks, host screens, signage, mobile, web, receipts, and even the audit log. Numbers, dates, currency, and PDF rendering all follow the chosen locale. The bilingual baseline glossary entry expands on what "full RTL" rules out — for example, a screen that simply mirrors English layout without re-grouping form fields and labels does not qualify.

How does the QMS integrate with Temenos, Finacle, or Mambu?

Production-grade integrations exist for all three. The typical surface area is customer-identifier lookup, account-status read, AML/KYC flag read, and event publication when a ticket is issued, called, or completed. A counter-only integration is light; a wealth-banker appointment integration that writes back into the core is heavier. Scoping honestly in Discovery is the most useful thing the implementation team can do.

Can the QMS consume the national identity gateway when our bank gets access?

Yes. The right pattern is OIDC over TLS to the gateway with attribute mapping into the QMS customer record. The QMS does not store the gateway's authoritative identity; it stores the minimum verified attributes the workflow needs and a reference. This is the same posture used for federated identity at banks in KSA and UAE.

What is a realistic Discovery price and timeline for an Omani bank?

Discovery for a 15-40 branch bank lands in the £15k-£40k band over four to six weeks. For a 50-80 branch enterprise programme with multiple lines of business, expect £25k-£60k over six to ten weeks. Discovery should produce a CBO-aligned architecture document, a PDPL data-flow map, a per-branch hardware budget, and a fixed-fee Build proposal that the investment committee can approve in a single sitting.

How big is the production portfolio that backs this advice?

Zeour ships into 1,247+ branches across 40+ countries — including the Omani government-bank programme in the OQBI Oman case study, the Kuwait National Bank London deployment, the Aljanoob Bank reference, and equivalent deployments across banking. That number is the credibility floor under every claim here.

Where does on-premises AI fit into the QMS?

The interesting AI surfaces are wait-time prediction, customer-routing optimisation, no-show prediction, and bilingual free-text feedback summarisation. All four can be delivered with open-weight large language models running on the bank's hardware — Llama, Mistral, Mixtral, Qwen, or DeepSeek hosted via vLLM, Ollama, or TGI. The data stays in the bank; the model stays in the bank; the audit trail is local.

What does the exit window mean in practical terms?

The exit window is the 90-day period at the end of the engagement during which the bank takes full operator self-sufficiency — source code, deploy keys, runbooks, and integration credentials are handed over, and a final assisted-run confirms independence. Combined with a fixed-fee engagement, this is the contract pattern that prevents vendor lock-in from becoming the largest line item in year three.

Where Zeour fits

Zeour Ltd is a UK-registered enterprise platform company shipping queue management, virtual queueing, online appointment, self-service kiosk, digital signage, visitor management, customer feedback, and wayfinding into 1,247+ branches across 40+ countries — with regional strength in GCC and MENA. In Oman, the production reference is the government-bank programme in the OQBI Oman case study; the wider regional posture is reflected in the Kuwait National Bank London and Aljanoob Bank deployments.

The Zeour posture is on-premises by default, bilingual English and Arabic with full RTL at the framework layer, contracted under fixed-fee engagements with an explicit 90-day exit window, and extensible across queue management, virtual queue, online appointment, self-service kiosk, digital signage, visitor management, and customer feedback. Across the wider banking industry practice, the same platform underpins programmes from London retail banking to GCC government banks. Sibling GCC posts — KSA banks, UAE banks, and Kuwait banks — describe the same posture adapted to each jurisdiction. If your Omani bank programme is in planning, the pricing reference and a direct conversation are the fastest way to test whether this is the right platform for your branch network.

---

Written by Zeour Engineering — published May 17, 2026. Zeour Ltd is a UK-registered enterprise platform company.