European queue management used to be a fairly uniform conversation — bank branch, retail till bank, hospital outpatient. In 2026 it is not. Different European markets sit at different points on the digital-front-door curve, run under different procurement frameworks, and answer to different data-residency expectations. A queue management deployment that works on a Madrid retail floor needs material adjustments before it lands well at a Stockholm tax office or a Berlin clinic. Here is a working read on the regional landscape and what shifts when you cross a border.

The UK: retail-led, NHS-paced, council-fragmented

The UK queue management market is the most mature in Europe by deployment volume, but it is also the most fragmented on the buyer side. Retail chains run their own enterprise deals — Boots, Argos, the supermarket banks for click-and-collect. The NHS runs trust-by-trust, with each trust treating queue management as a clinic-flow problem first and a CX problem second. The buyer is operational, the spec is HL7 and FHIR adjacent, and the timeline is whatever the trust's IT change board says it is. Local councils run council-by-council; some still on paper, some on cloud-only SaaS, some on on-prem.

Practical implication for vendors: there is no single UK go-to-market motion that covers all three. We run retail and NHS through different sales conversations, with different reference architectures and different reference deployments. The SpaceNK retail deployment sits on one side of this; the public-sector deployments — including the Romanian consulate in Birmingham UK and the Kuwait National Bank office in London UK — sit on the other. The cross-border reference deployments are interesting because they show the same platform handling a consular flow in one location and a wealth banking flow in another, both inside the UK but with very different operational tempos.

DACH (Germany, Austria, Switzerland): on-prem-first, slow, durable

DACH buyers — public sector and enterprise alike — still default to on-premises wherever the workload touches personal data, which in queue management is everywhere. This is not a 2022 conversation; it remains true in 2026. The procurement cycles are longer (frequently 9 to 18 months from first contact), the security review is deeper (you will be answered with a 60-page IT-Grundschutz questionnaire), and the contract conditions are sharper, but a deployment that lands stays for years.

What works: a sovereign on-prem deployment with strong audit, German-language UI for all operator-facing surfaces, and signed data-processing agreements that name a German or Swiss data plane. What does not work: cloud-only pitches, US-data-plane pitches, or anything that cannot be air-gap-deployed if requested. The DACH security review is also the most thorough in Europe — vendors who have not invested in a documented secure development lifecycle, an incident response playbook, and a vulnerability disclosure programme will not pass the first stage.

Nordics (Sweden, Denmark, Norway, Finland): digital-mature, cloud-pragmatic, English-friendly

The Nordics are the opposite of DACH in posture. Digital maturity is high, English-language operations are normal, and cloud-pragmatic deployments (often Azure West Europe or AWS Stockholm) are well-accepted in public-sector and healthcare buyers. The differentiator here is not sovereignty — it is integration depth into existing digital-citizen platforms (BankID, the eIDAS-aligned national IDs, the digital-first municipal stacks).

Queue management that lands well in the Nordics integrates cleanly into the digital-first citizen flow — appointment booking via the city portal, identity confirmed via BankID, queue ticket delivered to the citizen's national digital wallet. Vendors who ship as standalone kiosk-only deployments will struggle. The Nordic public-sector buyer is operating a citizen journey that spans several systems, and the queue management deployment is expected to be one well-integrated node in that journey rather than an island.

France: procurement-heavy, accent on user experience, sovereignty mid-tier

France runs queue management through a procurement culture that is closer to the GCC than to the UK — heavy RFP, heavy compliance posture, and a real preference for European or French-flagged data planes when sovereignty matters. UX expectations are high, particularly on the consumer-facing surfaces (mobile virtual queue, kiosk UI), and French-language coverage is non-negotiable for any public-sector deployment.

What works: a polished French-language deployment with strong UX, an SOC 2 plus GDPR posture, and ideally a Franco-European data-plane story. The hyperscaler offering OVHcloud is increasingly cited in public-sector procurement. The French enterprise buyer has slightly different expectations from the public-sector one — more flexibility on data plane, less on UX — but both expect the deployment to feel native to the French market rather than translated from an English-first product.

Iberia and Italy: SaaS-pragmatic, retail-led, growing public-sector pull

Spain, Portugal, and Italy are the most SaaS-pragmatic of the southern European markets, with retail chains driving most of the queue management deployment volume in 2026. Public-sector adoption is growing — Italian regional health authorities are increasing investment in clinic-flow management, Iberian municipal services are catching up to Nordic citizen-portal patterns — but the pace varies sharply by region.

What works in these markets: a SaaS deployment with strong local-language coverage (Spanish, Portuguese, Italian, plus regional variants like Catalan or Basque where the operator runs in those autonomies), and a pricing posture that fits Iberian SME procurement (smaller commit, monthly billing). What does not work: enterprise-only sales motions priced for the FTSE-100 buyer. The southern European buyer is sensitive to commercial flexibility in a way the DACH and Nordic buyers are not.

Malta: digital-government showcase, public-sector dense

Malta sits outside the usual European groupings but punches above its weight as a reference market for digital-government queue management. Servizz.gov Malta, MFCR Malta, and the Ministry of Transport Malta all run on the GLARUS queue management ecosystem. The deployment pattern is small footprint, high integration depth, English-and-Maltese language coverage, and a digital-first citizen flow that joins appointment booking, identity, and queue arrival in a single journey. The reference value is disproportionate to the market size.

What the Malta deployments demonstrate at the procurement level is that a small national operator can run a fully integrated digital-citizen flow on a queue management deployment that would be the envy of a large municipality elsewhere in Europe. The architecture is replicable; the political will to integrate is what is harder to replicate.

What the regulators care about, in plain English

Across all of these markets, three regulatory threads are consistent in 2026.

GDPR is the floor — every deployment needs Article 6 lawful basis documented, Article 9 special-category handling for any health-adjacent flow, Article 30 records of processing, and an explicit DPIA for anything touching biometrics or behavioural analytics. Vendors who treat GDPR as a tick-box are about to be cut from public-sector shortlists.

The NIS2 directive is now in force across the EU member states, which means queue management deployments touching essential or important entities (energy, transport, public administration, certain banking and healthcare functions) carry mandatory cybersecurity baselines, board-level governance, and incident-reporting timelines. The vendors who land in regulated environments need a documented incident response playbook, a tested communication procedure, and a board-aware governance model.

The EU AI Act is in transitional enforcement — relevant for any queue management deployment that uses AI for behavioural prediction (wait-time forecasting, peak-load estimation), which falls into the limited-risk or transparency-obligation tiers depending on implementation. The transparency notice for a model-driven feature is no longer optional.

Practical implication: any 2026 European queue management spec needs a DPIA template, a NIS2 incident-reporting hook, and an AI-Act transparency notice for any model-driven feature. Vendors who do not ship these are about to be cut from procurement shortlists across the EU.

What we have shipped recently

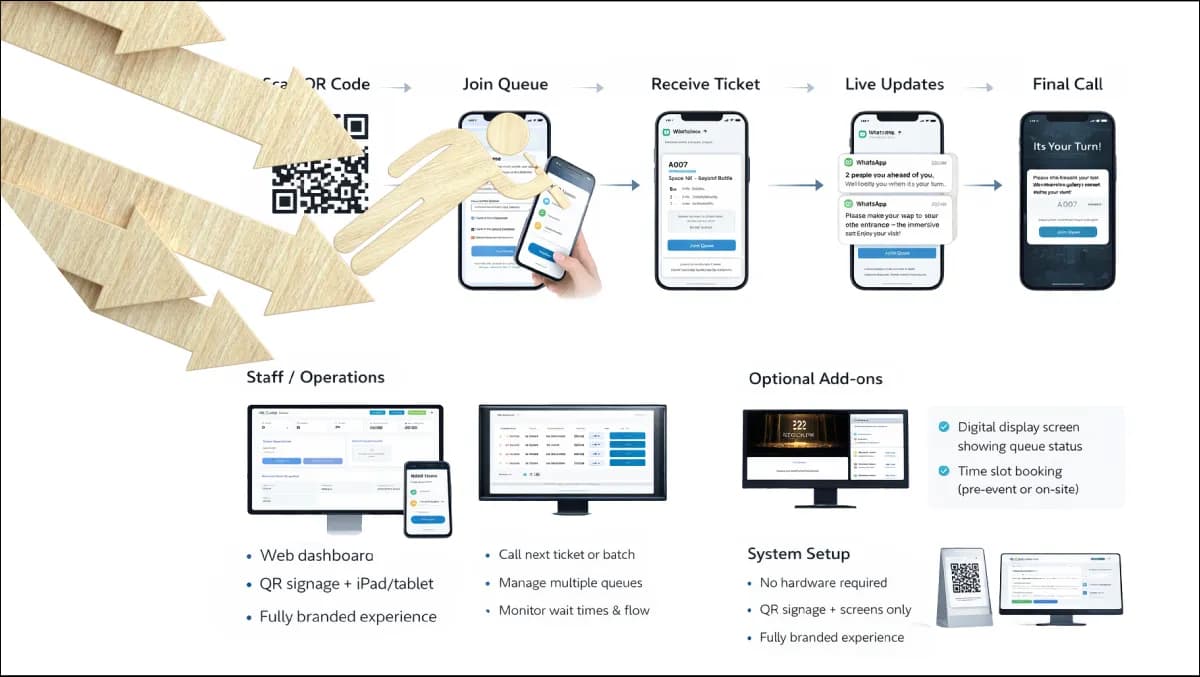

The Queue Management line within GLARUS has live European deployments across Malta, the UK, and broader EU markets in 2026, alongside the wider GCC, MENA, Americas, Africa, and Asia install base that anchors the product line. The European deployments share the same code base as the rest — what changes is the language pack, the data-plane configuration, the compliance posture, and the integration adapters for the local identity, payment, and clinical-flow systems. Re-localising the same stack to a new European market is a configuration project, not a re-engineering project.

If you are running a 2026 European queue management procurement and want a no-pitch read on what is shipping, what is not, and what the GLARUS architecture would look like in your environment — that is what the first scoping call is for.